State-Mandated Retirement Savings Programs

and Upcoming Deadlines in NY and NJ

By Charles C. Shulman, Esq.

I. Background, DOL Interpretive Bulletin 2015-02

A. State Mandated Retirement Savings Programs Enacted in a Number of States. In the past 10 years, a number of states have enacted laws requiring private employers to facilitate a state-mandated retirement savings arrangement if they don’t already offer one. The most common model is the payroll-deduction auto-IRA (generally a Roth IRA). These are usually structured as a Roth IRA. Most of these programs default to an initial contribution rate set between 3% and 5%. Employers can remain exempt if they choose to establish their own private retirement plans like a 401(k).

B. Interpretive Bulletin 2015-02. The Department of Labor set forth guidance in 2015 that enabled state-mandated retirement savings programs. DOL Interpretive Bulletin 2015-02, DOL Reg. § 2509.2015-02, 80 Fed. Reg. 71936 (Nov. 18, 2015), provide guidance on how states can sponsor or facilitate retirement programs without violating ERISA preemption. It notes that states act as market participants when they offer voluntary options. These models include (i) marketplace platforms to connect businesses with private plans and payroll deduction IRAs, (ii) state-sponsored prototype plans, or (iii) multiple employer plans where the state serves as the lead sponsor. Such programs are generally permitted if participation is voluntary and they don’t interfere with the uniform administration of private benefit plans. The bulletin explicitly distinguishes these ERISA-covered models from the auto-IRA models that many states now mandate.

II. States With Mandated Retirement Savings Programs

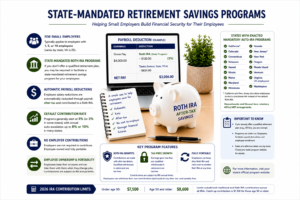

A. 17 States with Enacted Mandatory Auto-IRA Programs. Currently, there are at least seventeen states with active or upcoming mandatory auto-IRA programs for covered employers. These states include California, Colorado, Connecticut, Delaware, Hawaii, Illinois, Maine, Maryland, Minnesota, Nevada, New Jersey, New York, Oregon, Rhode Island, Vermont, Virginia and Washington State.

B. Most of 17 States Use Just a Roth IRA; Employee Threshold Between 1 and 25. The auto-IRA is generally a Roth IRA, although several states, including California & NJ, also allow a traditional IRA option. The employee threshold is generally 1, 5 or 10 employees (in Virginia, 25 employees). In NYS, affiliated employers under IRC § 414 are aggregated.

C. In 17 States, Initial Deferral 5% or 3% and Some with Auto-Escalation. In most of the states the initial contribution is 5%, but in some, e.g., CT, NJ & NY it is 3%. Most contain an annual 1% escalation up to 8 or 10%.

D. States with Voluntary IRA Programs. New Mexico has a voluntary IRA and Roth IRA program. Pennsylvania and Georgia are considering auto-IRA programs.

E. States with 401(k) MEP. Massachusetts has a voluntary 401(k) multiple employer plan (MEP) for small nonprofits , and Missouri is launching a voluntary 401(k) MEP for businesses with 50 or fewer employees.

F. States With No Mandatory Retirement Savings Program. The remaining states, e.g., Texas, Florida, Ohio, either have no active mandates or have only recently begun considering legislation without passing laws.

G. No Employer Contribution; Same Limit as Individual IRAs. The state mandated or voluntary savings programs prohibit employer matching or non-elective contributions. The annual contribution limit for the state IRAs or Roth IRAs in 2026 is $7,500 for individuals under age 50, and $8,600 for those 50 or older.

H. Exemption for Partial Qualified Plan Coverage. An employer doesn’t need to cover all workers to be exempt from these mandates. The exemption for sponsoring a qualified plan applies even if it covers some, but not all, employees. Official guidance in California, Delaware, Hawaii, Illinois, Maine, Minnesota, New Jersey and New York specifically confirms this partial coverage rule. Minnesota and New Jersey explicitly note this includes employers who merely contribute to a multiemployer trust fund for union employees. Commentators assume that the other states with mandatory auto-IRA programs also operate under the same entity-level structure exemption for maintaining or contributing to qualified plan for some employees and would also exempt employers that contribute to multiemployer plans to which the employer contributes to.

I. IRAs are Portable; Distribution Age. These accounts are fully portable. Employees keep their savings and can transfer the accounts even if they change jobs. Funds can be rolled into other IRAs. However, IRS regulations do not permit rolling Roth IRA funds into an employer-sponsored 401(k). Participants can withdraw their Roth IRA including investment earnings tax-free and penalty-free at age 59 1/2 and after a five-year holding period. To withdraw non-Roth amounts without the 10% early distribution penalty, the participant generally must be at least age 59 1/2. The participant will still be subject to ordinary income tax on the distribution of these non-Roth amounts.

III. New York Secure Choice Savings Program

A. New York Secure Choice Savings Program with Roth IRAs for Employers With 10 or More Employees that do Not Otherwise Participate in a Qualified Retirement Plan. New York State initially enacted its NYS Secure Choice Savings Program in 2018 as a voluntary option for employers with under 100 employees. New York later amended the law in October 2021 to make participation mandatory for covered employers. Following several implementation delays, the program officially launched in October 2025. An employer is a covered employer in New York if the employer (i) employed 10 or more workers in the state at all times during the previous calendar year, (ii) has been in business for at least two years, and (iii) the entity has not offered a qualified retirement plan in the preceding two years. An employer should formally certify its exemption on the state portal at https://www.newyorksecurechoice.com if it already sponsors a qualified plan.

B. Roth IRA Only; 3% Deferral Rate; No Auto-Escalation. For New York only the Roth IRA is available. The initial contribution is 3% of total pay. There is no auto-escalation, although employees may elect an annual escalation or higher contribution percentages up to 10%. Employees can opt out or choose different elections at any time. Employers cannot make matching contributions and cannot contribute to the plans.

C. Under the New York Secure Choice Savings Program, the 10 Employee Threshold Would Also Include Controlled Group Affiliates of the Employer. New York General Business Law, Article 43, Section 1300, regarding the NYS Secure Choice Savings Program, defined “employer” as an entity with 10 or more employees engaged in a business, industry, profession, trade, or other enterprise in New York state, whether for profit or not for profit. Section 1300 also provides that all terms carry the same meaning as used in comparable contexts in the Internal Revenue Code. It is generally assumed that this will include the controlled group rules of IRC §§ 414(b) and (c) and the affiliated service group rules of IRC § 414(m). Other states do not specifically incorporate controlled group aggregation rules.

D. If Qualified Plan Offered Only to Part of Workforce Such as Union Employees. New York General Business Law Article 43, Section 1300(4) provides an exception from NYS Secure Choice mandate the employer has “offered a qualified retirement plan, including, but not limited to, a plan qualified undersections 401(a), 401(k), 403(a), 403(b), 408(k), 408(p) or 457(b) of the Internal Revenue Code of 1986 in the preceding two years. See also, https://newyorksecurechoice.zendesk.com/hc/en-us with details on this.

In https://tinyurl.com/NY-exemption-partial-plan the NYS SECURE SAVINGS Program answers the question: I already offer a 401(k) or other qualified retirement plan to some employees but not all. Do I have to offer this program too?” And the answer given is “No, if you offer an employer-sponsored retirement plan to any of your employees, you can certify your exemption, and you will not need to facilitate the program.” Commentators assume that the same should be true if the employer contributed to a multiemployer pension or 401(k) plan for only the union employees and nonunion employees were not covered by a plan.

E. Portability and Investments. The NYS Secure Choice Roth IRA is fully portable from employer to employer. New York initially places funds in a Conservative Principal Protection Fund for 30 days. It then moves the funds to a Target Retirement Date Fund based on an assumed retirement age of 65, unless another fund is selected by the employee.

F. New York Enrollment Deadlines – the Latest is July 15, 2026. New York enrollment deadlines are: for employers with 30 or more employees, March 18, 2026; for employers with 15 to 29 employees, May 15, 2026; and for employers with 10 to 14 employees, July 15, 2026.

G. Potential Penalties in NYS. In NYS, lack of compliance with the NYS Secure Choice Savings Program mandates, start with a warning in the first year, and could reach (i) $250 per employee in the second year, (ii) $500 in the third year, and (iii) $1,000 per employee in subsequent years. Specific failure-to-register penalties may still be under review.

IV. NJ Secure Choice Savings Program – RetireReady NJ

A. RetireReady NJ Program – Threshold Lowered to 10 Employees in Jan. 2026. New Jersey enacted its Secure Choice Savings Program Act on March 28, 2019, codified in N.J.S.A. 43:23-13 through 32. It was amended on January 20, 2026. NJ P.L. 2025, c. 379. The NJ program launched on June 30, 2024. NJ Secure Choice Savings Program was rebranded as RetireReady NJ prior to the launching. The mandate originally covered employers with 25 or more employees.

B. Enrollment Deadline in NJ for 25+ Employees Was in Nov. 2024, Future Deadline for 10+ Employees TBD. The registration deadline for employers with 25 or more employees passed on November 15, 2024. The January 2026 amendment reduced the employer threshold in NJ from 25 to 10 employees. Once implemented, employers with 10 or more workers will be required to participate if they have operated for two years and lack a qualified plan. The employer should formally certify its exemption on the state portal at retireready.nj.gov if it already sponsors a qualified plan. New Jersey does not incorporate controlled group rules, and an entity-by-entity determination can be made.

C. Default Roth IRA at 3% With Auto-Escalation. Employers cannot make matching contributions and cannot contribute to the plans. New Jersey savers may choose either a Roth or a traditional IRA, though the Roth IRA is the default option. NJ sets a default employee contribution rate of 3% of gross pay, but the 3% initial rate automatically escalates by 1% each January until it reaches a 10% cap. Employees can opt out entirely at any time.

D. Exemption for Offering of a Qualified Plan Just to Union Employees Or Just to Some of Employees?New Jersey RetireReady exempts employers that already offer their own retirement savings plan, as stated in https://tinyurl.com/NJ-exemption-if-has-qual-plan. The NJ webinar FAQs at https://tinyurl.com/NJWebinarFAQs states that (i) an employer is entirely exempt if they offer an employer-sponsored plan to any portion of their workforce, (ii) contributing to a union retirement plan exclusively for union members satisfies this requirement, and (iii) the employer isn’t required to be the primary plan sponsor or offer the plan to all employee.

E. Portability; Target Date Funds; Withdrawals. RetireReady NJ accounts are fully portable from employer to employer. New Jersey relies primarily on various targeted market-based investments similar to target date funds. You can roll the funds into another IRA. However, IRS rules generally don’t permit rolling Roth IRA funds into an employer 401(k). Participants can generally withdraw their own IRA or Roth IRA contributions at any time without tax or penalty. Withdrawing investment earnings usually requires a qualified distribution. To avoid income tax and a 10% additional tax, the participant generally must be at least age 59 1/2 and have held the account for a five-year period.

F. NJ Penalties. New Jersey issues a written warning in the first year of noncompliance. It then fines employers (i) $100 per employee in the second year, (ii) $250 in the third and fourth years, and (iii) $500 from the fifth year onward.