Charles C. Shulman, Esq. has over 20 years of experience in ERISA, employee benefits and executive compensation law. Before starting his own firm, Charlie practiced at Paul Weiss, at Cahill Gordon & Reindel and at Skadden Arps. He is admitted in New York and New Jersey, and may be reached at cshulman@ebeclaw.com, 212-380-3834 or 201-357-0577.

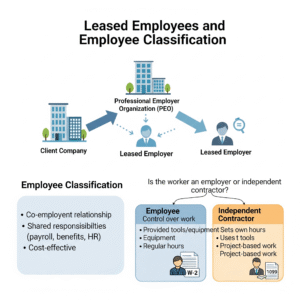

An issue that has recently attracted attention has been misclassification of employees as independent contractors. Government agencies are auditing companies for worker misclassification. Leased employees from professional employer organizations (PEOs) are also subject to examination as to whether the leased employees are really employees of the client companies—with the client companies being either co-employers with the PEO or being the sole employer. This article reviews the state of the law of leased employees and what can be done to minimize any liabilities. The following issues are discussed: (i) examination of PEOs for worker misclassification; (ii) joint employment by client company and PEO or employees of just of the client company; (iii) main criteria for employee status, including under the Darden test whether the company has the right to control manner and means by which work is accomplished, or the criteria under the economic realities test; (iv) a 2002 revenue procedure with IRS presumption that employees of PEOs should be treated as being the employees solely of the client companies; (v) Section 530 of the Revenue Act of 1978—safe harbor where there was a reasonable basis for worker classification; (vi) whether workers are leased employees as defined in IRC § 414(n)—and impact of leased employee status on testing; (vii) Microsoft “inoculation” language; (viii) cases re worker classification in leasing organizations; and (ix) consequences of misclassification.

Much attention has been focused recently on misclassification of employees as independent contractors. A number of federal and state agencies are auditing and investigating companies for worker misclassification. To some extent, leased employees from leasing companies—often referred to as professional employer organizations (“PEOs”)[1] —are also being examined as to whether the leased employees are actually employees solely of the client companies or are employees of both the PEOs and the client companies.

The main test for employee status is whether the company has the right to control manner and means by which work is accomplished, although other factors also play a role. A 2002 revenue procedure shows an IRS presumption that employees of professional employer organizations may really be the employees solely of the client companies.

Sometimes a PEO and client company will be found to be co-employers, in which case the impact on payroll tax should not be significant since the PEO already collected the payroll tax. Other times, however, the client company may be found to be the sole employer, in which case the amount of payroll tax already collected was not from the employer and could be collected (with penalties) from the true employer (although presumably by the nonemployer could file for a refund).

Even if leased employees are not found to be common-law employees of the recipient company, if they are leased employees as defined in IRC § 414(n), they would also have to be aggregated for nondiscrimination coverage testing (but not for nondiscrimination in contributions or benefits, assuming the plans exclude leased employees). Leased employee under § 414(n) would include where services are provided pursuant to agreement, person has performed such services for the service recipient on a substantially full-time basis for a period of at least one year, and the services are performed under the primary direction or control of the service recipient.

Consequences of misclassification could include payment for retroactive FICA, FUTA, state unemployment and workers compensation if the leased employees are found to be employees only of the client company and not of the leasing company. Overtime pay may be required if the reclassified employee is non-exempt. Retroactive union benefits may be required where applicable. In terms of having to retroactively include reclassified employees in the client companies’ employee benefit plans, this can often be avoided by specifically excluding reclassified employees from retroactive inclusion in the plan. If determined to be leased employees as defined in § 414(n), the company would have to retroactively test its qualified plans fornondiscrimination coverage, although leased employees would not have been included in the plans, assuming the plans exclude leased employees .

See detailed discussion below.

1. Increased Focus on Employee Classification

Crackdown on Employees Misclassified as Independent Contractors

Over the last few years there has been increased focus on employees misclassified as independent contractors. The IRS has increased its audit activity and has also announced that it would conduct audits of 6,000 randomly selected companies in 2010.[2] President Obama’s fiscal year 2011 budget allocated almost $25 million for IRS and DOL audits and enforcement regarding misclassified workers.

New York established in 2007 a Joint Enforcement Task Force on Employee Misclassification coordinating efforts between six agencies, and has uncovered in its first 16 months approximately $157 million in unreported earnings, $5 million in unemployment taxes, $12 million in unpaid wages and in excess of $1 million in workers’ compensation.[3]

Leasing Organization (PEO) and Client Company May Be Reclassified as Joint Employers or Client Company Alone May Be the Employer

Most of the audit activity is focused on workers classified as independent contractors, as this involves significant revenue because of the loss with respect to independent contractors of social security/Medicare tax, unemployment tax, state workers’ compensation, overtime payments, etc. For workers employed by leasing organizations, the above taxes and expenses will presumably have already been paid by the leasing organization. Thus, even if determined that the recipient company is a co-employer with the leasing company there would not be significant liability, since the leasing organization as employer has presumably already withheld income tax and paying FICA, FUTA, state unemployment and workers compensation.[4] However, even in a leased employee context, the workers may be losing out on benefits (unless misclassified employees are specifically excluded from benefits in all events) and the workers may be unfairly excluded from joining or forming a union at the recipient company.

In certain instances, however, worksite/leased employees will be reclassified as employees solely of the recipient company and not of the leasing organization at all.[5] In such cases the government may seek payment with interest and penalties from the real employer, with the leasing organization required to file for refund of such payments.

2. Reclassification as Employee – “Darden” Standard; Microsoft Case

“Darden” Standard—Common-Law Definition for ERISA—Right to Control Manner and Means by Which Work Is Accomplished

The Supreme Court in Nationwide Mutual Insurance Co. v. Darden,[6] has ruled that for purposes of ERISA employee is defined as a “common-law” employee, and that “[i]n determining whether a hired party is an employee under the general common law of agency, we consider the hiring party’s right to control the manner and means by which the product is accomplished.”

The Court lists the following other factors that are also relevant to this inquiry including: (1) the skills required; (2) the source of the instrumentalities and tools; (3) the location of the work; the duration of the relationship between the parties; (4) whether the hiring party has the right to assign additional projects to the hired party; (5) the extent of the hired party’s discretion over when and how long to work; (6) the method of payment; (7) the hired party’s role in hiring and paying assistants; (8) whether the work is part of the regular business of the hiring party; (9) whether the hiring party is in business; (10) the provision of employee benefits; and (11) the tax treatment of the hired party.[7] Thus, one must examine an arrangement primarily to see that the recipient company does not control or have the right to control the manner and means by which the work is accomplished. The other factors listed are not dispositive, but should be evaluated to see if the contemplated arrangement will have favorable or unfavorable factors.[8]

Common-Law Definition Also Adopted in Payroll Tax Regulations

See Treas. Reg. § 1.3121(d)-1(c) which applies the Darden standard, as well as other factors to FICA (Social Security/Medicare) tax. It provides:

(1) Every individual is an employee if under the usual common law rules the relationship between him and the person for whom he performs services is the legal relationship of employer and employee. (2) Generally such relationship exists when the person for whom services are performed has the right to control and direct the individual who performs the services, not only as to the result to be accomplished by the work but also as to the details and means by which that result is accomplished. That is, an employee is subject to the will and control of the employer not only as to what shall be done but how it shall be done. In this connection, it is not necessary that the employer actually direct or control the manner in which the services are performed; it is sufficient if he has the right to do so. … Other factors characteristic of an employer, but not necessarily present in every case, are the furnishing of tools and the furnishing of a place to work, to the individual who performs the services. (Emphasis added)[9]

20 Factors in Rev. Rul. 87-41 Which Has Been Combined Into Three Categories

The IRS in Rev. Rul. 87-41, regarding payroll tax, provides twenty factors that have been identified in rulings or cases as indicating whether sufficient control is present to establish an employer-employee relationship, including: whether an employee must comply with instructions about when, where and how to work; training; integration of the person’s services into the business operation; services rendered personally; hiring, supervising and payment of assistants; continuing relationship; set hours of work; full time requirement; doing work on the premises; order or sequence set by employer; oral or written reports; payment by hour, week, or month; reimbursement of business or travel expenses; furnishing of tools; significant investment; realization of profit or loss; not working for more than one employer; services not available to the general public; right to discharge; and right to quit.

These twenty factors have been broken down in IRS guidance to three categories: behavioral control (whether there is a right to direct or control how the worker does the work, i.e., receiving extensive instructions on how work is to be done and training about required procedures and methods), financial control (whether there is a right to direct or control the business part of the work—having significant investment in the work, not being reimbursed for business expenses and ability to realize a profit or incur a loss all point to being an independent contractor) and relationship between parties (what does the contract say; are there employee benefits).[10]

If the worker classification is unclear, Form SS-8, Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding can be filed with the IRS.[11]

Section 530 of the Revenue Act of 1978 Relief—Where Reasonable Basis for Worker Classification

Section 530 of the Revenue Act of 1978, as amended[12] provides an employer with relief from Federal employment taxes with respect to workers who have been reclassified as employees, if (1) the employer has consistently treated similar workers as independent contractors, (2) there was a reasonable basis for doing so, and (3) federal tax returns including Form 1099s are consistent with such treatment.[13]Reasonable basis requires reasonable reliance on case-law, prior audits and industry standard.

On audit the IRS will often challenge whether there really was reasonable basis for the classification and will examine closely to see if Form 1099s were filed and whether similar workers were always treated the same.[14] Also, an audit of employee classification can lead to an expanded IRS audit of other issues with the employer.

Section 530 is not directly applicable to leased employees, but it does show a Congressional intent to not reclassify employees who are classified on a reasonable basis, and this can apply to leased employees as well.

Vizcaino v. Microsoft—Employees Reclassified Will Require Retroactive Benefits Unless Have Microsoft Inoculation” Language in Plans

One of the major risks of employee misclassification is that the employee may be retroactively entitled to employee benefits. In Vizcaino v. Microsoft,[15] , the Ninth Circuit held that freelancers at Microsoft who were found by the IRS to be misclassified as independent contractors but were in fact common-law employees, and were therefore entitled to benefits under the company’s retirement savings plan, employee stock purchase plan and stock option plan which were provided to all “employees.”[16]

In light of this Ninth Circuit case, recently plans have added “Microsoft inoculation” provisions which state that persons originally classified by the company as independent contractors are not eligible under the plan even if later reclassified by the IRS, until the date of the reclassification determination. Similarly, with regard to leased employees. The client company plans should specifically exclude leased employees from participation even if they are aggregated for nondiscrimination coverage testing purposes.

4. Case-Law and Rulings Regarding Professional Employer Organizations

Ninth Circuit Case—Where PEO Exerts Only Illusory Control over Leased Employees They Are Not PEO’s Employees and Cannot Remain in its Plan

In Professional & Executive Leasing, Inc. v. Commissioner,[17] the Ninth Circuit ruled that where a leasing company hired employees, covered the employees under the leasing company’s benefit plans and leased their services to various recipients, for purposes of the exclusive benefit rule of IRC § 401(a)(2), the employees were not employees of the leasing company, primarily because the leasing company exercised no meaningful control over them. The court based its conclusion on the facts including that: (1) the leasing company never exercised its right to reassign workers;(2) the leasing company had no reason to reassign or fire a worker unless a recipient complained, an unlikely scenario because most workers had some control over the recipient to which they were leased through employees’ equity ownership in the recipient;(3) the leasing company’s control over the workers’ salaries was illusory, because any change required approval by either the recipient or the worker; and (4) the leasing company did not conduct any screening of the workers except to verify their licenses to practice.

The court also noted that the recipient companies rather than the leasing company, provided the equipment, tools and office space for the workers, furnished the workers with malpractice insurance, and controlled the details of how and when work was to be performed.

Therefore, the court held that the employees were really employees of the recipient companies and not the leasing company, and therefore participation by such employees in the leasing company’s retirement plans would violate the exclusive benefit rule of IRC § 401(a)(2) that a plan of an employer must be for the exclusive benefit of its employees.

If a leasing company exercises meaningful control over the workers, the workers are not significant shareholders of the leasing company, the leasing company has control over salaries and screens the workers as any company hiring an employee will do, workers would probably not be a common-law employee of the client company.

Six Factor Economic Realities Test Used in Second Circuit Co-Employer Case

In a 2003 Second Circuit case, Zheng v. Liberty Apparel Co.[18]—which involved a garment company which hired subcontractors who in turned hired garment workers to stitch and finish pieces of clothing, and whether the company was a “joint employer” with the subcontractors—the court applied a six factor economic realities test to determine if the company was a joint employer of the subcontractors’ workers:

(1) whether the company’s premises and equipment are used for the workers’ work; (2) whether the subcontractors that hired the workers has a business that can or does shift as a unit from one putative joint employer to another; (3) the extent to which the workers perform a discrete line-job that is integral to the company’s process of production; (4) whether responsibility under a contract between the subcontractors and the company could pass from one subcontractor to another without material change; (5) the degree to which the company or its agents supervise the employees’ work; and (6) whether the employee works exclusively or predominantly for the company.[19]

Rev. Proc. 2002-21—Employees of PEO Are Actually Employees of Recipient Company, and Each Employer Must Sign Onto Leasing Company’s 401(k) Plan

Rev. Proc. 2002-21, as amplified by Rev. Proc. 2003-86, provides that professional employer organizations (PEOs) that maintain a defined contribution plan must treat the plan as a multiple-employer plan. Citing the cases of Darden and Professional & Executive Leasing, the IRS acknowledges the complexity involved in the determination of whether a leased employee is the common law employee of the PEO or of the client organization, and provides a framework under which plans sponsored by PEOs will not be treated as violating the exclusive benefit rule solely because they provide benefits to the leased employee. The relief offered is for the PEO either to terminate its plan or to convert its plan into a multiple employer plan IRC § 413(c), and avoid possible violation of the exclusive benefit rule of IRC § 401(a)(2).

This revenue procedure evidences the IRS’ bias towards finding employees of professional employer organizations to be employees solely of the service recipient companies and not of the PEOs. However, if a leasing company maintains primary control over the employee and the Company does not maintain the primary control, and some of the other criteria also point to ownership, the presumption of Rev. Proc. 2002-21 should be negated. Note also that the revenue procedure only deals with retirement plans sponsored by the professional employer organization and not retirement plans of the service recipient company.

PEO Health Plans as MEWAs

If employees of a PEO are characterized as common law employees of the client companies, the PEO health plan would be a multiple employer welfare arrangement (“MEWA”). MEWAs have limited ERISA preemption under ERISA§ 514(b)(6). MEWAs are subject to state insurance laws regarding required reserves and contributions. This can create an issue for self-insured plans. With insured plans, however, the insurance company presumably already meets the reserves and contributions requirements.

See, DOL Information Letter (Mar. 1, 2006),[20]that the PEO and its clients would not be considered a single employer even if the PEO had agreements with each of its clients under which the PEO has an option to purchase an 80% interest in each client company, since the options arrangements are really shams. Therefore the MEWA issue was not avoided in that case.

For self-insured MEWAs the state insurance reserves and contributions laws would effectively shut down the MEWA. For insured MEWAs the insurance company already should be satisfying the reserves and contributions requirements, but a DOL Form M-1 filing would be required for both types of MEWAs, whether insured or self-insured. ERISA § 101(g) and DOL Reg. § 2520.101-2 require MEWAs to file annual Form M-1 with the DOL (with $1000 a day penalties under ERISA § 502(c)(5) for failure to file).

This is a very common area of noncompliance, as PEOs may be aware of Rev. Proc. 2002-21 but are often not aware of the MEWA requirements.

Right to Discharge Employee as a Factor in Determining Employee Classification

Note that Treas. Reg. § 1.3121(d)-1(c) regarding Social Security and Medicare withholding provides that: “The right to discharge is also an important factor indicating that the person possessing that right is an employer.”

However the legislative history regarding changes made by the Small Business Job Protection Act of 1996 to IRC § 414(n)(2)(C) (adding primary direction and control language to definition of leased employee) states: “Factors that generally are not relevant in determining whether such direction or control exists include whether the service recipient has the right to hire or fire the individual and whether the individual works for others.”[21]

The above regulation and legislative history can perhaps be reconciled as follows. If the determination is whether the worker is an employee or independent contractor like in the FICA regulations, right to discharge is an important factor indicating that the person possessing that right is the employer. However, in the leased employee situation in determining whether the company is the employer or the leasing organization is employer, whether the service recipient company has the right to hire or fire the individual is not relevant because even a nonemployer client of a PEO would want the right to remove a leased worker if not satisfied with the work.

Case Holding that Leased Employees Were Legitimately Classified as Employees of the Leasing Company

In Castiglione v. U. S. Life Insurance Co.,[22] the court found that a leasing company, rather than the company to which the leasing company leased employees, was the employer for purposes of an ERISA plan. The company to which employees were leased had entered an employee leasing contract with the leasing company, wherein the leasing company agreed to ensure the recipient company’s adherence to federal, state, and local tax laws, payroll, workers’ compensation laws and to provide group health and life insurance. In honoring this agreement the leasing company purchased several insurance policies for employees. The court noted that ERISA § 3(5) merely requires a leasing agency to act “directly as an employer or indirectly in the interests of an employer, in relation to an employee benefit plan.” The court found that the leasing agency was the employee’s direct employer in relation to the employee benefits plan, even though it did not control the employee’s day to day activities. In addition, in any event it would be no less than an indirect employer.

Leasing Organization for Only One Company

A professional employer organization that services numerous companies (e.g., Administaff, ADP, Paychex, Trinet, etc.) is less likely to be attacked as illusory, than an organization set up for solely one employer. It is easier to demonstrate that a large professional employer organization exerts sufficient control independent of the client company with respect to its employees when there are numerous clients and employees are sent on varying assignments for varying periods of time.

5.If Primarily Under Direction and Control of Company Then Treated As § 414 (n) Leased Employee and Must Be Aggregated for Testing

There are two ways that leasing company employees would be required to be tested together with company employees for nondiscrimination testing. First, if found to bea common-law employee of the company then the employeemust be included in nondiscriminationtesting (and for participation as well unless specifically excluded from the plan based on their status or based on the classification the employer gave to them at the time). Second, even if not a common-law employee of the company if they are leased employees as defined in IRC § 414(n) as described below, they would also have to be aggregated for testing (but not for participation, assuming the plans exclude leased employees). [23]

Leased Employees Under § 414(n) Must be Aggregated with All Company Employees for Nondiscrimination Testing

Under IRC § 414(n), a leased employee as defined in § 414(n) is treated as an employee of the service recipient.

IRC § 414(n)(3) requires that a leased employee as defined in § 414(n) be treated as an employee of the service recipient for the following requirements: (1) the general nondiscrimination requirements of IRC § 401(a)(4) and the ADP/ACP nondiscrimination requirements of IRC §§ 401(k)(3) & 401(m)(2) (unless the leased employees are specifically excluded by the document from participation); (2) the minimum participation requirements of IRC § 401(a)(26); (3) the minimum coverage requirements of IRC § 410; (4) the top-heavy requirements of IRC § 416; and (5) the maximum benefit and annual addition requirements of IRC § 415.

Leased Employee Under § 414(n) Defined as Service Provider for One Year or More Where Services Are Performed Under Primary Direction or Control of Service Recipient

“Leased employee” is defined in IRC § 414(n)(2) as any person who is not an employee of the service recipient and who provided services to the recipient company if: (1) such services are provided pursuant to an agreement between the service recipient and the leasing organization, (2) such person has performed such services for the service recipient on a substantially full-time basis for a period of at least one year, and (3) such services are performed under the primary direction or control of the service recipient.

Criteria for Determining Whether Services Are Performed Under Primary Direction or Control of Service Recipient—Similar to Common-Law Employee Definition

See legislative history to the Small Business Job Protection Act of 1996 § 1454, which provides: “Whether services are performed by an individual under primary direction or control by the service recipient depends on the facts and circumstances. In general, primary direction and control means that the service recipient exercises the majority of direction and control over the individual. Factors that are relevant in determining whether primary direction or control exists include whether the individual is required to comply with instructions of the service recipient about when, where, and how he or she is to perform the services, whether the services must be performed by a particular person, whether the individual is subject to the supervision of the service recipient, and whether the individual must perform services in the order or sequence set by the service recipient. Factors that generally are not relevant in determining whether such direction or control exists include whether the service recipient has the right to hire or fire the individual and whether the individual works for others.”[24] Note that as defined by the Conference Report, the “primary direction or control” test of IRC § 414(n)(2) is similar to the common-law employee test that service recipient has the right to control and direct the individual as to the details and means by which the work is accomplished. However, it could possiblynot be a common law employee because the recipient company does not have the right to control the details and means by which the work is accomplished, but nevertheless the worker is under the primary direction and control of the recipient company under § 414(n)(2).

6. Consequences of Misclassification of Leased Employees; Self-Audit

As discussed above, the consequences of misclassification of independent contractors would trigger obligations for income tax withholding, and payment of FICA, FUTA, state unemployment and workers compensation. However, in the case of worksite/leased employees, if the entities are treated as co-employers and in all events the government will receive payments from one of the parties, and the company recipient is treated as the sole employer, the government may collect from the employer and the leasing company will have to seek a refund for amounts paid.

If the IRS considers the recipient company to be co-employer with the leasing organization but not sole employer, since the government has already collected income tax withholding, FICA, FUTA, state unemployment and workers compensation from the leasing company, the government will generally not seek a duplicate payment from the recipient company since a co-employer has already paid the amount

The adverse consequences of reclassification of leased employees as employees of the recipient company or as § 414(n) leased employees is that there may be retroactive benefits claims under the company’s benefit plans, although if the plans specifically exclude those misclassified (or determined not to be leased employees as defined in § 414(n)) until reclassified, this won’t be a problem.

If reclassified or if determined to be leased employees as defined in § 414(n), the company would have to retroactively test its qualified plans fornondiscrimination taking into account that the leasing company employees have not been included in the plans—and since they are non-highly compensated employees the company would likely fail the nondiscrimination tests.

An additional, adverse impact could occur if the addition of employees to the company would bring it over the threshold for certain employment laws.[25]

A company that has leased employee arrangements where the company exerts a significant amount of control over the leased employee, such that the company may be the employer or co-employer, should conduct self-audit to determine if the treatment of the employees as employees of the PEO is proper. The audit should be done with or under the direction of legal counsel in order to retain attorney-client privilege.

[4]See, e.g., Rev. Rul. 66-162, (sales clerks were employees of both the concessionaire who leased space at a department store and the department store); Chief Counsel Adv. Memo. 200415008 (PEO and clients were co-employers and where PEO went bankrupt, client company could be eligible for employment taxes);Chief Counsel Adv. Memo. 200017041 (FICA/FUTA wage base applicable to staffing company and clients as co-employers)

[5]See, e.g., Professional & Executive Leasing, Inc. v. Commissioner, 862 F.2d 751 (9th Cir. 1988) (discussed below, and holding that where a leasing company leased employees to various companies, the employees were not employees of the leasing company at all and therefore the leasing company violated the exclusive benefit rule of IRC § 401(a)(2) by including such employees in the leasing company’s plans.)

[7] 503 U.S. at 323–324 (emphasis and format added).

[8] See, however, Second Circuit Zheng decision below applying a six factor “economic realities” test in a co-employer case.

[9] The same definition is used in Treas. Reg. § 31.3401(c)-1(b), regarding income tax withholding, and Treas. Reg. § 31.3306(i)-1(b), regarding FUTA federal unemployment.

[13] There has been proposed legislation to repeal or amend Section 530.Recent proposed legislation regarding worker classification include the Taxpayer Responsibility, Accountability and Consistency Act (S. 2882), and The Fair Playing Field Act of 2010 (H.R. 6128), both of which would repeal Section 530.

[23] IRC § 414(m) affiliated service rules could be applicable if the owners of the service organization are also employees or shareholders of the recipient company.

[25] For example, 15 employees are required for application ofthe Americans With Disabilities Act andTitle VII, 20 employees for the Age Discrimination in Employment Act and COBRA, 50 employees for the Family and Medical Leave Act, 100 employees for WARN Act, etc.