ERISA’s “Controlled Group” Rules – A Timely Review

By CHARLES C. SHULMAN, ESQ.

Printed in 51 Journal of Pension Planning and Compliance, no. 1, at 1 (WK, Fall 2025)

https://tinyurl.com/erisa-controlled-group-rules

This article: explains how controlled-group entities are treated as a single employer under the Code and ERISA for purposes including Title IV liability, qualified plan nondiscrimination, Code § 409A, COBRA, cafeteria plans, and the ACA employer mandate; reviews recent case law and SECURE 2.0 attribution changes effective in 2024; analyzes the parent-subsidiary and brother-sister controlled-group tests with examples; examines complex ownership-attribution rules (including options, spousal and family attribution, and SECURE 2.0 clarifications); discusses potential personal liability of 80% owners operating unincorporated trades or businesses; and surveys recent private-equity cases addressing the “investment-plus” standard and partnership-in-fact theories.

Under the Internal Revenue Code (“Code”) and the Employee Retirement Income Security Act (“ERISA”), employees of certain related “controlled group” entities, as defined in §§ 414(b) & (c) of the Code, are treated as employed by a single employer, for purposes of liability under Title IV of ERISA, for qualified plan nondiscrimination testing under the Code and for other purposes listed below.

These rules are not new, but this article includes changes made by the SECURE 2.0 Act of 2022, first effective in 2024, and an August 2025 case and other recent cases regarding private equity investment-plus ownership and potential partnership-in-fact ownership.

This article is broken into four parts: (i) applicability of controlled group rules and parent-child and brother-sister tests; (ii) controlled group attribution rules for option holders, 5% owners and family members; (iii) controlled group liability issues re individual owners with an unincorporated trade or business; and (iv) controlled group liability issues with portfolio companies of multiple private equity owners.

Note that under Code § 414(m), employees of certain entities that are part of an “affiliated service group” are also treated as employed by a single employer, for purposes of nondiscriminatory coverage testing under the Code (but not for liability under Title IV of ERISA). These rules were also amended by the SECURE 2.0 Act. The “affiliated service group” rules under Code § 414(m) will be discussed in a separate upcoming article.

1. Applicability of Controlled Group Rules and Parent-Child and Brother-Sister Tests

Controlled Group Tests

There are two alternate tests to determine controlled group status under the Code and ERISA: (i) a parent-subsidiary controlled group test; and (ii) a brother-sister controlled group test.

Applicability of Controlled Group Rules

It is often incorrectly assumed that the ERISA controlled group rules are only applicable for purposes of ERISA Title IV (defined benefit plan) liability; but, in fact, controlled group rules are also relevant in a host of contexts (some affecting defined contribution plans or nonqualified plans as well).

Controlled group rules under ERISA and related laws apply for: (i) Title IV pension termination liability under ERISA § 4062(a); (ii) ERISA § 4069(a) (transaction with a principal purpose to evade pension termination liability); (iii) PBGC premiums under ERISA §§ 4006 & 4007 (§ 4007(e)(2)); (iv) minimum funding obligations under Code § 412 (§ 412(c)(11)(B)); (v) Code § 4971 excise tax for failure to meet minimum funding (§ 4971(e)(2)); (vi) PBGC lien for unpaid contributions exceeding $1 million (ERISA § 303(k)); (vii) single employer plan distress termination where all members of the controlled group must be in financial distress under ERISA § 4041; (viii) multiemployer pension plan withdrawal liability (ERISA §§ 4201(a) & 4001(b)(1)); (ix) Code § 404(a) limits on deductions (Code § 404(a) & (g)); (x) qualified plan nondiscrimination rules, primarily with respect to the minimum coverage tests under Code § 410(b), the defined benefit plan minimum participation tests under Code § 401(a)(26), the general test for contributions and benefits under Code § 401(a)(4) regulations, the benefits, rights and features under Treas. Reg. § 1.401(a)(4)-4 and certain other nondiscrimination and qualification rules that could be affected by a controlled group affiliate (Code §§ 414(b) & (c)); (xi) simplified employee pension nondiscrimination test under Code § 408(k)(3); (xii) Code § 409A limitations on nonqualified deferred compensation plans (for purposes of the definition of service recipient, the determination of when a separation from service occurs, plan aggregation rules, and the six-month delay for specified employees of public companies) (Code § 409A(d)(6)); (xiii) COBRA continuation coverage (ERISA § 607(4); Code § 414(t)); (xiv) cafeteria plan nondiscrimination tests of Code § 125, self-insured medical reimbursement nondiscrimination test of Code § 105(h), and certain fringe benefit nondiscrimination tests in Code § 132 (Code §§ 414(t), 105(h)(8) & 125(g)(4)); and (xv) Affordable Care Act mandated coverage rules for employers with 50 or more employees on a controlled group basis, to provide affordable healthcare benefits or pay certain penalties under Code § 4980H(a) & (b).[1] The WARN Act also has inter-corporate liability if companies are so intertwined in their affairs that they appear separate but are actually part of a single enterprise (caselaw interpreting 29 U.S.C. § 2101(a)(1)).[2]

ERISA controlled group rules would NOT apply to, e.g., (i) prohibited transactions, (ii) other excise taxes, (iii) consequences of plan disqualification, [3] (iv) Title I reporting and disclosure obligations, or (v) contractual liabilities for promised benefits, etc.

Parent-Subsidiary Controlled Group Test

Parent-subsidiary test. A parent-subsidiary controlled group will exist if there is a chain of entities conducting trades or businesses that are connected through a ”controlling interest” with a common parent, with controlling interest defined: (i) in the case of corporation as at least 80% of the total combined voting power of all classes entitled to vote OR at least 80% of the total value of all shares of the subsidiary; (ii) in the case of a trust or estate an 80% actuarial interest in the trust or estate; (iii) in the case of a partnership (or other entity taxed as a partnership) an 80% interest in profits OR capital of the partnership; and (iv) in the case of a sole proprietorship 100% ownership of the trade or business. Code § 1563(a)(1) referenced by Code § 414(b); Treas. Reg. § 1.414(c)-2(b)(2).

Voting power. Voting power under Code §§ 414(b) & 1563(a)(1) means the power to control the corporation’s business through the election of the board of directors, as illustrated in various cases and rulings.[4]

Parent-child controlled group not applicable if individual owns the other entities, but there is no entity that owns the other entities. Parent-child controlled group would not apply if an individual (not a trade or business) owns the other entities. If an individual owns individually 80% in several entities, but there is no entity that owns the other entities, and it’s not the individual’s trade or business that owns the other entities but rather the individual. However, the brother-sister controlled group, discussed below, would likely pull the entities owned by the individual into a single controlled group.

Section 415 50% Standard. For purposes of the Code § 415 limitations on qualified plan benefits and contributions, the controlling interest for purposes of the parent-subsidiary test is reduced from 80% to 50%. Code § 415(h); Treas. Reg. § 1.415(a)-1(f).

Parent-subsidiary example 1: Partnership A owns stock having 80% of the total combined voting power of all classes of stock entitled to vote of Corporation B. Partnership A also owns 80% of the profits interest in Partnership C. Partnership A is the common parent of a parent-subsidiary controlled group of trades or businesses consisting of Partnership A, Corporation B, and Partnership C. See Treas. Reg. § 1.414(c)-2(e) Ex. 1. See also, Treas. Reg. § 1.1563-l(a)(2)(ii) Ex. 1 & 2.

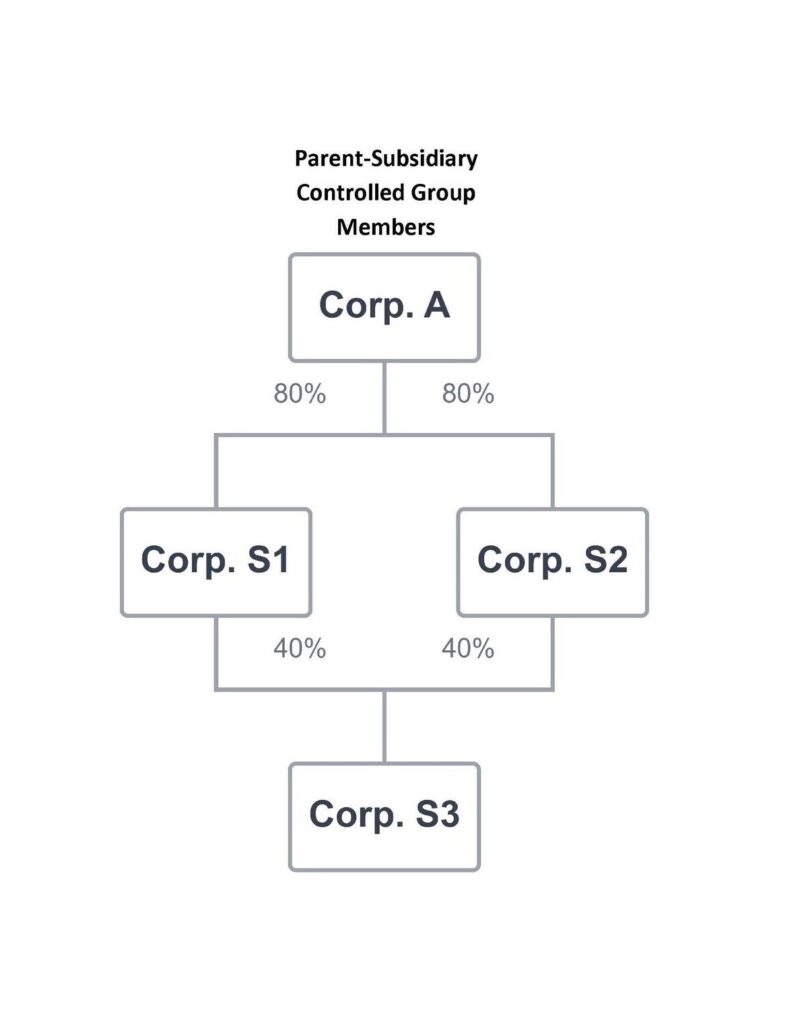

Parent-subsidiary example 2: Corporation A owns 80% of the only class of stock Corporation S1 and of Corporation S2. Corporations S1 and S2 each own 40% of the only class of stock of Corporation S3. Corporation A is the common parent of a parent-subsidiary controlled group consisting of corporations A, S1, S2 and S3 (with the indirect 40% ownership interests of Corporation S3 combined). See diagram below. See also, Treas. Reg. § 1.414(c)-2(e) Ex. 2, and Treas. Reg. § 1.1563-l(a)(2)(ii) Ex. 3.

Exclusion of certain remaining ownership interests in parent-subsidiary test for 50% owned entities. Certain ownership interests are excluded in determining the parent-subsidiary controlled group. Specifically, if the parent owns (a) 50% or more of the vote or value of subsidiary corporation, (b) 50% or more of the actuarial interest of subsidiary trust or (c) 50% or more of the profits or capital of subsidiary partnership, then any remaining ownership interest in the subsidiary will be ignored if the remaining interest is held by (i) principal owner, officers, partners or fiduciaries of the parent, (ii) employees of the subsidiary if subject to a “put” to employer on termination of employment or other substantial restriction, (iii) a trust which is part of a deferred compensation plan of foreign affiliates or (iv) controlled tax-exempt organizations. Ignoring the remaining ownership interest will have the effect of increasing the parent’s ownership interest in the entity, and if the increased ownership interest is 80% or more of the entity, it could bring the parent and subsidiary entity it into a parent-subsidiary controlled group. Code § 1563(c)(2)(A); Treas. Reg. § 1.414(c)-3(b).

Brother Sister Controlled Group Test

Brother-sister test. A brother-sister controlled group exists where there are two or more trades or businesses which meet two tests: (i) the same five or fewer persons who are individuals, estates or trusts[5] commonly own together 80% or more of “control,” as defined above, in each of the entities; and (ii) these five or fewer individuals, estates or trusts also own together 50% or more of the “identical” ownership (effective control) in the entities, with identical ownership meaning that ownership is taken into account only to the extent it is identical with respect to each of the entities (i.e., one looks only at the lowest percentage ownership in any of the common entities and count only that lowest percentage ownership). Code § 1563(a)(2); Treas. Reg. § 1.414(c)-2(c).

Thus, the brother-sister test includes an 80% common (combined) control component and a 50% identical ownership component. Under the identical ownership component, if corporations X, Y and Z are partially owned by individual A with a 20%, 30% and 40% interest, respectively, the identical ownership interest that is counted for individual A is only 20%.

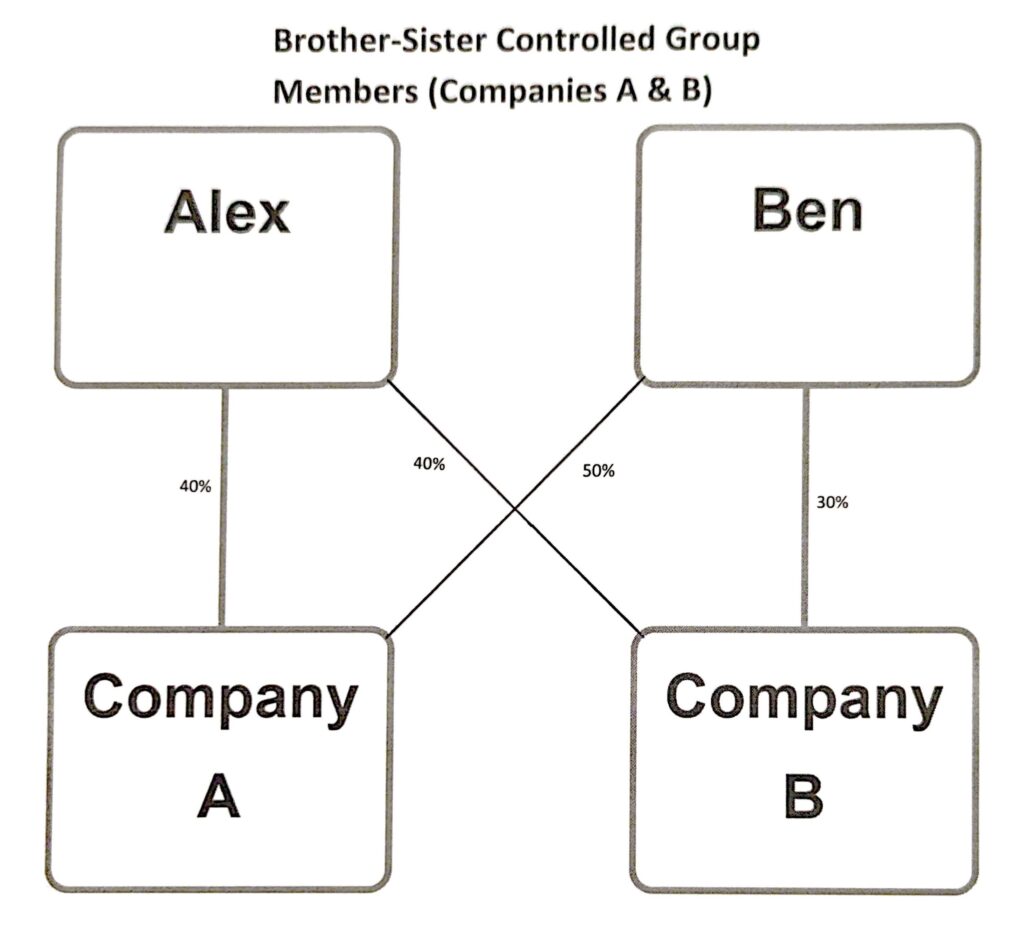

Example of brother-sister test. Record the ownership percentage of each person in the group across all companies. Determine each person’s lowest ownership percentage across all of the companies (the identical ownership).

| Individuals | Company A | Company B | Identical Ownership |

| Alex | 40% | 50% | 40% |

| Ben | 50% | 30% | 30% |

| Total | 90% (common control equals or exceeds 80%) | 80% (common control equals or exceeds 80%) | 70% (identical ownership exceeds 50%) |

Company A and B are in a brother-sister controlled group since (1) five or fewer individuals commonly own at least 80% of each of the entities (in the above example Company A is commonly owned 90% by Alex and Ben, and Company B is commonly owned 80% by Alex and Ben, both of which equal or exceed 80%); and (2) when adding up identical ownership in each entity, i.e., the lowest percentage ownership by each individual in each company, the identical ownership exceeds 50% (in the above example Alex’s identical ownership in both companies A & B is 40% and Ben’s identical ownership in both companies A & B is 30%, thus yielding identical ownership by Alex and Ben of 70% of both companies, which exceeds 50%). See diagram below. See also, examples in Treas. Reg. § 1.414(c)-2(e) Ex. 4 and Treas. Reg. § 1.1563-l(a)(3)(iii) Ex. 1.

Brother-sister test excludes stock ownership of individuals who do not hold an interest in each of the entities under Vogel Rule. Under the Supreme Court case of U.S. v. Vogel Fertilizer Company, 455 U.S. 16 (1982), stock ownership of individuals who do not hold an interest in all of the entities is disregarded even for the 80% component of the brother-sister test. The Court in Vogel found that the statutory term “brother-sister controlled group” connotes a close horizontal relation between the corporations, suggesting the same persons must satisfy the 80% ownership requirement for each corporation. Analyzing the structure of the statute, the Court noted that “five or fewer persons” is the conjunctive subject for both the 80% test and the 50% test. This structural parallel led the Court to deduce that the 80% test must also require common ownership among the shareholders used for the 50% test. The Court invalidated prior Treas. Reg. § 1.1563-1(a)(3), rejecting its “singly or in combination” language. The Court highlighted that the Treasury Department’s representations before Congress explicitly included a common ownership requirement in the 80% test, making the “singly or in combination” language of those regulation contradictory to those initial proposals. This Vogel clarification has been incorporated into the more recent version of Treas. Reg. § 1.1563-1(a)(3), which provides in § 1.1563-1(a)(3)(ii)(C) that the five or fewer persons whose stock ownership is considered for purposes of the 80% requirement must be the same persons whose stock ownership is considered for purposes of the more-than-50% identical ownership requirement.

Example of application of Vogel Rule. For example, if the above example were expanded to include a third shareholder, Cathy, with a 20% interest in Company B but a 0% ownership in Company A, and other changes as shown below, we exclude Cathy’s ownership in both companies, even in Company B, since she does not have any ownership in Company A, and without counting Cathy’s 20% interest in Co. B, there is not common (combined) control of 80% or more in Company B, and therefore the brother-sister test for companies A and B is not met.

| Individuals | Company A | Company B | Identical Ownership |

| Alex | 70% | 70% | 70% |

| Ben | 30% [not counted under Vogel] | 0% | 0% |

| Cathy | 0% | 30% [not counted under Vogel] | 0% |

| Total | 70% (not including 30% of Ben since he does not have any identical ownership), so common control does not equal or exceed 80%) | 70% (not including 30% of Cathy under “Vogel” since she does not have identical ownership in the other entities, so common control does not equal or exceed 80%) | 70% (identical ownership exceeds 50%) |

The regulations as amended in Treas. Reg. § 1.414(c)-2(c)(1), 53 Fed. Reg. 6603 (March 2, 1988) provide, incorporating Vogel: “The term ‘brother-sister group of trades or businesses under common control’ means two or more organizations conducting trades or businesses if (i) the same five or fewer persons who are individuals, estates, or trusts own (directly and with the application of § 1.414(c)-4) a controlling interest [80% or more] in each organization, and (ii) taking into account the ownership of each such person only to the extent such ownership is identical with respect to each such organization, such persons are in effective control [more than 50%] of each organization. The five or fewer persons whose ownership is considered for purposes of the controlling interest requirement for each organization must be the same persons whose ownership is considered for purposes of the effective control requirement.”

Note that if Cathy was married to Alex, and ownership takes into account spousal ownership under Treas. Reg. § 1.414(c)-4(c), Alex may be deemed to own Cathy’s interest in Company B, but if Cathy had no interest, employment, management or restriction on sale role in Company B and Company B majority passive investments, Cathy’s ownership would not be attributed to Alex. Also, since Cathy has no interest in Company A, there would not be 80% common ownership in Company A, and therefore Companies A and B would not be brother-sister entities.

Exclusion of certain remaining ownership interests in brother-sister test for 50% owned entities

Certain ownership interests are excluded in determining brother-sister controlled group. Specifically, if five or fewer persons own 50% or more of an entity, the remaining ownership is ignored if held by (i) a qualified plan, (ii) employees of the entity if it is subject to substantial conditions (e.g., an asymmetrical right of first refusal), or (iii) controlled exempt organizations.

Combined Controlled Group Rule

Combined Controlled Group. There is also a combined group test under which a group of three or more organizations consists of at least one parent-subsidiary group, the parent of which is a member of a brother-sister group. Code § 1563(a)(2); Treas. Reg. § 1.414(c)-2(d).[6]

Example of combined controlled group. For example, Walter, an individual, owns a controlling interest in Partnership X and Partnership Y, and Partnerships X and Y together meet the requirements for the brother-sister controlled group. Partnership X also owns a controlling interest in Company Z meeting the requirements for the parent-subsidiary controlled group. Since Partnership X is the parent of a parent-subsidiary controlled group and is also a member of a brother-sister controlled group, Partnership X, Partnership Y and Company Z are members of the same combined controlled group. See Treas. Reg. § 1.414(c)-2(e) Ex. 8.

Other Issues Relating to Controlled Group Rules

Treasury stock and nonvoting preferred stock disregarded. In determining control for the parent-subsidiary or brother-sister controlled group tests, stock does not include treasury stock or nonvoting preferred stock. Code § 1563(c)(1)(A); Treas. Reg. § 1.414(c)-3(a). Thus, stock does not include (i) treasury stock reacquired and held by the company, or (ii) nonvoting stock that is limited and preferred as to dividends.[7]

Controlled group for tax-exempt organizations. In testing common control for tax-exempt organizations (where there is no ownership control), 2007 regulations provide that common control exists between tax-exempt organizations if at least 80% of the directors or trustees of one organization are either representative of, or directly or indirectly controlled by the other organization. Treas. Reg. § 1.414(c)-5(b), 72 Fed. Reg. 41128 (July 22, 2007) (revised § 403(b) regulations).[8]

Anti-Abuse rule in regulations. There is also an anti-abuse provision in the regulations for in the section dealing with tax-exempt organizations, but which would apply to other abuses in the controlled group area.[9]

Bankruptcy. On occasion courts have disregarded stock ownership in a bankruptcy context where there was no actual ownership.[10]

2. Controlled Group Attribution Rules for Option Holders, 5% Owners and Family Members

Attribution Rules for Option Holders. Constructive ownership in an entity can exist if there is an option to acquire a controlling interest of the entity. Code § 1563(e)(1); Treas. Reg. § 1.414(c)-4(b)(1).[11]

Courts split on whether option attribution rules can be used to diminish other shareholders’ interests.Courts are divided on the issue of whether the option attribution rule can be used to diminish other shareholder interests. Some courts and the PBGC hold that option attribution can be used to dilute other shareholder interests.[12] Other courts have taken the view that the option attribution rule may only be used to increase ownership of the optionee but not to dilute ownership of other shareholders.[13]

Attribution rules for 5% owners. For purposes of the parent-subsidiary and brother-sister tests, the following ownership attribution rules apply to corporations, partnerships and estates and trusts: If an individual owns 5% or more of an entity, the individual is deemed to own a proportionate part of any interests owned by that entity. Code § 1563(e)(2), (3) & (4) and Treas. Reg. § 1.414(c)-4(b)(2), (3) & (4).[14]

Spousal attribution rules and SECURE 2.0 Changes. For purposes of the parent-subsidiary and brother-sister tests, the following family attribution rules apply: an individual is deemed to own the interest in an entity that his or her spouse owns, provided that they are not divorced or legally separated. However, the spousal attribution rule does not apply where all of the following conditions are met: (i) the individual does not actually own any interest of the entity in which the spouse has an interest (hereinafter referred to as “such entity”), (ii) the individual is not a director or employee of such entity, (iii) the individual does not participate in the management of such entity, (iv) not more than 50% of such entity’s income is derived from passive sources (such as royalties, rents, dividends, interest and annuities), and (v) the spouse’s ownership in such entity is not subject to conditions which substantially restrict or limit the spouse’s right to dispose of such interest and which run in favor of the individual (or his or her minor children). Code § 1563(e)(5); Treas. Reg. § 1.414(c)-4(b)(5). Amendments made by the SECURE 2.0 Act of 2022 § 315 adding Code § 414(b)(2)(A), effective for plan years beginning after December 31, 2023, provide that where the individual and his or her spouse reside in community property states, the community property laws can be disregarded for purposes of the § 414(b) controlled-group rules.[15]

Minor child attribution rules and SECURE 2.0 Changes. An individual is deemed to own stock owned by his children under age 21. Code § 1563(e)(6); Treas. Reg. § 1.414(c)-4(b)(5). However, as provided by the SECURE 2.0 Act of 2022 § 315 adding Code § 414(b)(2)(B) & (C), effective for plan years beginning after December 31, 2023, despite the normal attribution of ownership to a minor child, a business owned by one parent and a business owned by the other parent (not subject to spousal attribution, e.g., by reason of legal separation or divorce or other reason) will not be considered to be in the same controlled group solely by reason of attribution to the minor child.[16]

Parent/child attribution rules. If an individual owns more than 50% of an entity, he or she is deemed to own any interests owned in that entity by his adult children, grandchildren, parents and grandparents. Code § 1563(e)(6)(B); Treas. Reg. § 1.414(c)-4(b)(6)(ii). There is no attribution rule for siblings.

3. Controlled Group Liability Issues re Individual Owners with an Unincorporated Trade or Business

Individual owners are generally not liable for a corporation’s ERISA liability. Generally, an individual owner or shareholder of a corporation are not liable for the corporation’s multiemployer withdrawal liability or single employer termination liability under the controlled group rules.[17]

Piercing Corporate Veil. One exception to the above rule, though, would be where the doctrine of piercing the corporate veil (alter ego) is applicable, for example, where there is fraud, disregard by the owner of the separate character of the corporation or shareholders undercapitalize the corporation.[18]

Liability of owner if owner engages in an unincorporated trade or business. Another important exception – where an individual owner (or shareholder if meeting a controlled group test) of a corporation could be held liable for the corporation’s ERISA termination or withdrawal liability – would be where the owner also engages in a trade or business as a sole proprietor (or partnership) and the unincorporated trade or business could make the owner individually liable for the corporation’s termination or withdrawal liability.[19]

Trade or Business. Neither ERISA nor the Treasury regulations define “trade or business.” Courts have generally adopted the standard articulated in the1987 Supreme Court case of C.I.R. v. Groetzinger, where the Court held that in the context of Code § 162, to be engaged in a trade or business, the taxpayer must be involved in the activity with continuity and regularity and that the taxpayer’s primary purpose for engaging in the activity must be for income or profit; sporadic activity, a hobby, or an amusement diversion does not qualify.[20] Several cases have applied Groetzinger in the ERISA context.[21]

Personal liability by reason of having unincorporated home business activity. A number of courts have found shareholders liable by reason of some business activity they engaged in as a sole proprietor, trust or partnership.[22] See below regarding private equity funds that engage only in passive investing.

4. Controlled Group Liability Issues re Portfolio Companies of Multiple Private Equity Owners

Whether private equity funds are a trade or business. As discussed further in this section, only “trades or business” under common control are treated as part of an ERISA controlled group. As discussed above, under the Groetzinger standard, to be engaged in a trade or business, the individual must be involved in the activity with continuity and regularity and that the taxpayer’s primary purpose for engaging in the activity must be for income or profit; but sporadic activity, a hobby, or an amusement diversion do not qualify.[23] With regard to private equity funds, historically, practitioners had generally taken the view that since they are generally passive investment vehicles with no employees and minimal involvement in day-to-day operations, they are not trades or businesses, and therefore separate portfolio companies owned by a private equity fund would not be in the same ERISA controlled group. However, the PBGC in a 2007 PBGC Appeals Board Opinion stated that a private equity fund that owned 80% or more of the portfolio company was a trade or business, because it was engaged in an activity with the primary purpose of income or profit and conducted business through an agent (the general partner) who managed fund investments on a regular basis.[24] According to this ruling, 80%-owned portfolio companies of a private equity fund would generally be in the same ERISA controlled group, and only in the unusual case where the facts and circumstances indicate that the private equity fund does not meet the Groetzinger standard for a trade or business, it would not be a controlled group.[25]

Investment plus, e.g., investment advisory and management services. A 2010 Eastern District of Michigan case, Board of Trustees, Sheet Metal Workers National Pension Fund v. Palladium Equity Partners, found the 2007 PBGC Appeals Board Opinion to be persuasive and “investment plus” is a trade or business. However, since there was more than one private equity investment funds and neither owned 80% of the portfolio company alone, there was still a genuine issue of material fact as to whether the three funds constituted a partnership or joint venture in fact.[26] A more recent August 2025 Western District of Missouri case found liability on the part of limited partnership investor in bankrupt companies, which had triggered withdrawal liability, since the limited partnership investor was more than a passive investor, since it actively managed the portfolio companies (investment-plus).[27]

Partnership-in-fact. Regarding when multiple funds constitute a partnership in fact, Luna v. Commissioner, 42 T.C. 1067 (1964) established eight factors to consider: (i) the agreement of the parties and their conduct in executing its terms; (ii) the contributions, if any, which each party has made to the venture; (iii) the parties’ control over income and capital and the right of each to make withdrawals; (iv) whether each party was a principal and coproprietor, sharing a mutual proprietary interest in the net profits or losses, or whether one party was the agent or employee of the other, receiving for his services contingent compensation in the form of a percentage of income; (v) whether business was conducted in the joint names of the parties; (vi) whether the parties filed Federal partnership returns or otherwise represented that they were joint venturers; and (vii) whether separate books of account were maintained for the venture; and (viii) whether the parties exercised mutual control over and assumed mutual responsibilities for the enterprise.[28]

2013 Sun Capital case. A 2013 First Circuit case, Sun Capital Partners III, LP v. New England Teamsters & Trucking Industry Pension Fund, found the PBGC Appeals Board Opinion to be persuasive, and confirmed that private equity funds will be engaged in a trade or business for ERISA controlled group purposes if there is “an investment plus” by the fund, e.g., by reason of active involvement in management (as well as control) of the portfolio companies; but there was still an issue of material fact as to whether the funds would be considered a partnership-in-fact.[29]

2016 Sun Capital district court case. A later district court case of Sun Capital Partners held that (i) both funds (the Sun Fund IV with a 70% investment and Sun Fund III with a 30% investment) were trades or businesses, and (ii) there was common control under ERISA by reason of Fund III and IV being a “partnership in fact.”[30]

Reversal by First Circuit in 2019 Sun Capital Case. The First Circuit overturned this decision, however, in Sun Capital Partners III, LP v. New England Teamsters & Trucking Industry Pension Fund, 943 F.3d 49 (1st Cir. 2019), cert. denied, 141 S. Ct. 372 (2020), holding that there was not a partnership in fact because the fund documents did not state that they were a partnership, the funds had different investors, the funds filed separate tax returns and the funds did not always make parallel investments.[31]

Multiple fund structure. Private equity funds have often structured investment through multiple funds in part to keep ownership below 80%, and avoid ERISA controlled group liability, but there is still some uncertainty on the safety of relying on that structure because they may be trades or business and there may be a partnership-in-fact (although the 2019 First Circuit Sun Capital Partners case gives some comfort in that regard).[32]

Affiliated Service Group Rules

Under Code § 414(m), employees of certain entities that are part of an “affiliated service group” are also treated as employed by a single employer, for purposes of nondiscriminatory coverage testing and other qualified plan rules under the Code (but not for liability under Title IV of ERISA). The affiliated service group rules will be discussed in a separate article.

[1] Regarding Code §4980H guidance about controlled group, see definition of “applicable large employer” in Treas. Reg. §54.4980H-1(a)(16) (entity treated as a single “applicable large employer” with 50 FTEs under Code §§ 414(b), (c), (m) & (o)), examples in §54.4980H-2(d) (where entities are treated as a single applicable large employer) and Notice 2011-36 (all entities under Code §§ 414(b), (c) or (m) are to taken into account in determining whether there is an applicable large employer with 50 FTE employees)

When conducting due diligence about a company, it is important to examine not only if the company has or participates in Title IV plans, but also if any controlled group members may have or participate in such plans.

[2] Administaff Companies., Inc. v. New York Joint Board, Shirt & Leisurewear Division, 337 F.3d 454, 457–58 (5th Cir. 2003); Pearson v. Component Tech. Corp., 247 F.3d 471, 477 (3d Cir. 2001); Adams v. Erwin Weller Co., 87 F.3d 269, 271 (8th Cir. 1996); Chauffeurs, Sales Drivers, Warehousemen & Helpers Union Local 572 v. Weslock Corp., 66 F.3d 241, 245 (9th Cir. 1995).

[3] However, because the applicable sections relate to qualification of a retirement plan, failure to recognize the common or related ownership with the retirement plan sponsor and other corporations or businesses could result in disqualification of the plan from inception or in operation.

[4] Voting power under Internal Revenue Code §§ 414(b) & 1563(a)(1) and analogizing to Code § 1504 re 80% or 50% of the total combined voting power of all classes entitled to vote – means the power to control the corporation’s business through the election of the board of directors, as illustrated in numerous Federal case decisions. See, e.g., Yaffe Iron & Metal Corp. v. U.S., 78-1 U.S. Tax Cas. (CCH) ¶9314, 41 A.F.T.R.2d 78-1057 (W.D. Ark. 1978), affirmed, 593 F.2d 8324 (8th Cir. 1979), cert. denied, 444 U.S. 843 (with regard to the § 1563 requirement of 80% control as part of brother-sister test, Tax Court held that a stockholder’s voting agreement is relevant where the effect of an agreement is to vest to two individuals with over 80% of the combined voting power of all classes of stock; Eighth Circuit affirmed and cert. was denied); Central States, Southeast and Southwest Areas Pension Fund v. CLP Venture LLC, 760 F.3d 745 (7th Cir. 2014), cert. denied, 135 S. Ct. 964 (2015) (in a case involving multiemployer plan withdrawal liability, even though a common owner of two corporations owned only 73% of one of the corporations (rather than 80%), the court took into account an escrow agreement which gave the individual the right to direct voting of the remaining 27% of the stock and concluded that there was an ERISA controlled group for purposes of determining withdrawal liability); Erie Lighting Co. v. C.I.R., 93 F.2d 883, 885 (1st Cir. 1937); Rev. Rul. 69-126, 1969-1 C.B. 218 (participation in management of subsidiary through election of board is criterion of voting power; upheld by numerous rulings to non-section 1504 cases, e.g., PLR 8128073, PLR 8221112, PLR 7406211920A and GCM 35789); Alumax Inc. v. C.I.R., 165 F.3d 822 (11th Cir. 1999) (where 50% shareholder had right to four votes per share including right to elect board members, but for supermajority matters such as major corporate transactions the 50% shareholder only had one vote per share, and the board members elected by 50% shareholder likewise had limits on voting on supermajority corporate transaction issues and were limited by other directors’ power to delay their actions, the 50% shareholder did not have requisite 80% voting control for purposes of consolidated returns under Code § 1504); Hermes Consol., Inc. v. U.S., 14 Cl. Ct. 398 (1988) (with regard to Code § 269 voting power is determined not merely by record ownership but by the ability to approve or disapprove of fundamental changes in the corporate structure and the ability to elect the corporation’s board of directors).

[5] This would exclude ownership by partnership or corporations.

[6] The term combined group means any group of three or more organizations, if (i) each such organization is a member of either a parent-subsidiary group or a brother-sister group, and (ii) at least one such organization is the common parent organization of a parent-subsidiary group and is also a member of a brother-sister group. Treas. Reg. § 1.414(c)-2(d).

[7] With regard to “convertible” preferred stock, see Rev. Rul. 71-83, 1971-1 C.B. 268, which held that for purposes of Code § 1504 (which until 1984 was worded exactly as § 1563), nonvoting preferred stock that is convertible into voting common stock is still considered “nonvoting stock that is limited and preferred as to dividends” since at the time the test is made it is still nonvoting, and therefore should not be counted for the affiliated group rules. However, it is possible that for purposes of the Code §§ 414 & 1563 controlled group tests, since even stock options are considered stock under the option attribution rules, convertible preferred should also be included. See, Williams, “Multiple Corporations,” 55 Tax Management Portfolio § IV.A. On the other hand, the option attribution rule only applies with respect to options for outstanding stock, which is different than convertible preferred stock.

[8] A trustee or director is treated as a representative of another organization if that person is a trustee, director, agent or employee of the other organization. Treas. Reg. § 1.414(c)-5(b). A trustee or director is controlled by another organization if the other organization has the power to remove the trustee or director and designate a new trustee or director. Id. Whether there is the power to remove the trustee or director is a facts and circumstances determination.

[9] Treas. Reg. § 1.414(c)-5(f) (“If the Commissioner determines that the principal purpose of a transaction is to avoid the application of section 414(b) or (c), the Commissioner may treat the organizations involved in the transaction as if the transaction had not occurred, or may otherwise disregard the transaction or the ownership interests created by the transaction, and may treat the organizations as members of the same controlled group or as separate employers, whatever is appropriate to carry out the purposes of section 414(b) and (c)).

[10] In re Challenge Stamping and Porcelain Co., 719 F.2d 146 (6th Cir. 1983) (where company bought parent of sponsor of pension plan while sponsor was in Chapter 11 reorganization, but bankruptcy court then auctioned off sponsor rendering stock of parent of sponsor worthless, buyer of parent of sponsor was not liable for controlled group termination liability since owning 100% of parent of sponsor was meaningless since even at that time bankruptcy court had full control of sponsor). See similarly, PBGC v. Ouimet Corp., 711 F.2d 1085 (1st Cir.1983), cert. denied 464 U.S. 961 (1983) (where subsidiary went bankrupt and terminated underfunded plan after acquisition by controlled group that included another bankrupt subsidiary, termination liability was allocated only to the solvent group members, and not bankrupt corporations’ estates, since applying the bankrupt’s assets to PBGC’s liability would have reduced assets available to their creditors and inequitably benefited group members; court noted that ERISA provides a lien on 30% of the net worth, not asset value and a bankrupt corporation has negative net worth). See also, Sutherland v. C.I.R., 78 T.C. 395 (1982) nonacq. 1986-2 C.B. 1, 1986 WL 713548 (Tax Court has held that businesses which are unsuccessful and are ceasing to conduct operations are not required to be included under the Code § 414(b) or (c) test, since to do so would be to require the inclusion of an employer which will, in effect, be maintaining an impermanent plan since it will soon be going out of business).

See, however, Pension Benefit Guaranty Corp. v. East Dayton Tool and Die Co., 14 F.3d 1122 (6th Cir. 1994), cert. denied 513 U.S. 816 (PBGC sought enforcement that a holding company, the parent of a sponsoring employer in bankruptcy was responsible for unfunded benefit liabilities of employer’s pension plan; the court held that 80% control rule applied, even though holding company did not control voting rights of its stock in employer; Challenge Stamping, cited above, which held that in a bankruptcy case the stock purchaser never had actual control over the bankrupt employer that sponsored the pension plan for termination liability was different that this case, because here the holding company actually controlled the employer and its Plan for 2-1/2 years).

[11] Code § 1563(e)(1), made applicable by § 1563(d)(1)(B) (if any person has an option to acquire stock, such stock shall be considered as owned by such person); Treas. Reg. § 1.414(c)-4(b)(1) (if a person has an option to acquire any outstanding interest in an organization, such interest shall be considered as owned by such person). An option to acquire such an option will also be considered as an option to acquire such stock or interest. Id.

If the option to acquire stock is subject to contingencies, there would generally be no attribution. Central Transport, Inc. v. Central States, Southeast and Southwest Area Pension Fund, 640 F. Supp. 56 (E.D. Tenn. 1986), affirmed, 8 EBC 2519, 1987 WL 36010 (6th Cir. 1987; unpublished), cert. denied 484 U.S. 926 (1989) (no withdrawal liability under ERISA § 4201 since stock purchase agreement made conditional on federal approval was not an option under § 1563(e)(1) since it was contingent on federal approval and purchaser had no control over contingency, and therefore company was not in controlled group under rules of § 414(c) and § 1563). However, if the option is exercisable only after a period of time without any conditions, there would be option attribution. Rev. Rul. 89-64, 1989-1 C.B. 91 (where an option distributed by a company to an officer in redemption of the officer’s stock was only exercisable only after the lapse of a fixed period of time, it is still subject to option attribution under Code § 318(a)(4)).

There are several cases that specifically apply the option attribution rule in an ERISA context (all dealing with multiemployer withdrawal liability). Tri-State Rubber & Equipment, Inc. v. Central States Southeast & Southwest Areas Pension Fund, 677 F. Supp. 516 (E.D. Mich. 1987) (seven companies controlled by an individual are under common control under § 414(c) and have withdrawal liability under ERISA § 4201; person who had option to purchase stock was constructive owner of such stock under § 1563(c)(1)); IUE AFL-CIO Pension Fund v. Barker & Williamson, Inc., 788 F.2d 118 (3d Cir.1986) (withdrawal liability exists under § 4201 where parent owns 75% of stock of subsidiary since option to purchase remaining 25% falls within option attribution rule of § 1563(e)(1)); Chicago Truck Drivers, Helpers and Warehouse Workers Union (Independent) Pension Fund v. Brotherhood Labor Leasing, 950 F. Supp. 1454 (E.D. Mo. 1996), denial of reconsideration, 950 F.Supp.1454 (where there was purchase agreement for immediate acquisition of withdrawing company (Be-Mac) by shareholders of defendant companies, this was enough to cause Be-Mac to be in controlled group under option rule, even if a court had later invalidated the sale, since there were no contingencies in purchase agreement); Teamsters Pension Trust Fund of Philadelphia v. Brigadier Leasing Associates, 880 F. Supp. 388 (E.D. Pa. 1995) (unsigned draft agreement which gave withdrawing employer’s CFO an option to purchase the other owner’s interest in the corporation did not establish existing of a binding agreement, and therefore other entities owned by CFO were not in controlled group); New York State Teamsters Conference Pension and Retirement Fund v. Express Services, Inc., 426 F.3d 640 (2d Cir. 2005) right of first refusal held by principals of former participating employer in multiemployer pension plan with respect to possible affiliates did not establish constructive ownership over purported affiliates; although statute defining constructive ownership includes an option to acquire stock, a “right of first refusal” was not same thing as stock option and statute made no reference to rights of first refusal).

[12] For the view that the option attribution rule can be used to diminish other shareholder interests, see, Sorem v. C.I.R., 334 F.2d 275 (10th Cir. 1964) (in determining whether a redemption was substantially disproportionate there must be included the total unissued stock on which other shareholders have stock options under § 318(a)(4)); Henry T. Patterson Trust by Reeves Banking & Trust Co. v. U.S., 729 F.2d 1089 (6th Cir. 1984) (unissued stock which minority shareholders have an option to acquire must be treated as outstanding under § 318(a)(4), which thereby increases the denominator and allows the redemption to be not essentially equivalent to a dividend, thus benefiting the majority shareholder in allowing him capital gain rather than dividend treatment); Rev. Rul. 89-64, 1989-1 CB 91 (stock must be able to be acquired at the election of the shareholder if there exist no contingencies with respect to such election; redeemed shareholder’s option taken into account); Rev. Rul. 68-601, 1968-2 CB 124 (redeemed shareholder’s option, but not unrelated holder’s option are not affected by redeemed shareholder’s option).

[13] For the view that the option attribution rule cannot be used to dimmish other shareholder interests, see, Northwestern Steel and Supply Co., Inc. v. C.I.R., 60 T.C. 356 (1973) (unexercised stock option owned by minority shareholder cannot reduce ownership percentage of 80% shareholder under § 1563(e)(1) for purposes of surtax exemption; note that in this case the option was to acquire the outstanding shares held by the majority shareholder, rather than an option to acquire unissued shares); Rev. Rul. 68-601 (unrelated holder’s option not taken into account).

[14] See e.g., Paza Staffing Services, Inc. v. C.I.R., 751 Fed. Appx. 223 (3d Cir. 2018) (Third Circuit upheld Tax Court decision that an ESOP was disqualified for failing to cover non-highly compensated employees of a related corporation in violation of Code § 410(b) minimum coverage rules an individual sold all of the stock of his company Paza Staffing Services to a newly established ESOP in an ESOP buyout; he then assigned all the employees to Golden Gate, a company he owned, and then had Paza lease the five employees back from Golden Gate; even though the stock of the corporation held by the ESOP was not technically a member of the same controlled group, the court held that, as sole beneficiary of the ESOP, the owner of Golden Gate was the constructive owner of Paza under Code § 1563(d)(2) and (e)(3)(A), and therefore the two companies were members of the same ERISA controlled group, and the employees of Golden Gate were required to be covered by the ESOP in order to pass IRS nondiscrimination minimum coverage requirements; therefore the ESOP was disqualified).

[15] These provisions in the SECURE 2.0 Act of 2022 (Division T of the Consolidated Appropriations Act, 2023) signed Dec. 29, 2022, were originally intended to be effective for plan years beginning on or after December 29, 2022, but the IRS has delayed the effective date for the controlled group changes in the SECURE 2.0 Act to plan years beginning after December 31, 2023. The SECURE 2.0 Act also adds Code § 414(b)(3), that to the extent changes made in new Code § 414(b)(2) result in changes to the controlled group, the Code § 410(b)(6)(C) transition rule (which allows disregarding changes until the end of the plan year following the plan year of specific corporate events) applies until the end of the plan year following the affected plan year.

[16] SECURE 2.0 Act of 2022 § 315 adding Code § 414(b)(2)(B) & (C), with a delayed effective date to plan years beginning after December 31, 2023. Specifically, stock or interests of entities held by the parents that not attributed to the spouse under the spousal attribution rules, will not be attributed solely as a result of minor child attribution. New Code § 414(b)(2)(B). Likewise, stock or interests of separate entities held by each of the parents that would be attributed to a minor child by reason of minor child attribution, but is not subject to spousal attribution, will not cause the entities to be in the same controlled group solely because of the minor child attribution. New Code § 414(b)(2)(C).

[17] Connors v. Coal America, Inc., 7 Employee Benefits Cas. (BNA) 1300 (D.D.C. 1986) (individual who was officer and shareholder of corporation is not liable for multiemployer withdrawal liability where there was no allegation of a basis for piercing the corporate veil); DeBreceni v. Graf Bros. Leasing, Inc., 828 F.2d 877 (1st Cir. 1987) (no multiemployer withdrawal liability on controlling shareholders and officers); Debreceni v. Bru-Jell Leasing Corp., 710 F. Supp. 15 (D. Mass. 1989) (95% shareholder not individually liable for multiemployer withdrawal liability); Scarbrough v. Perez, 870 F.2d 1079 (6th Cir.1989) (indirect owner not liable for multiemployer withdrawal liability); Wilhelm v. McAnn’s W. 48th Street Restaurant Corp., 34 EBC 1659, 2004 WL 2658066, 34 (N.D. Ill. 2004) (a shareholder is not personally liable for multiemployer withdrawal liability of corporation; even N.Y. law does not hold a shareholder jointly and severally liable for post-dissolution debts of the corporation).

[18] See, e.g., the following court cases piercing the corporate veil: Lowen v. Tower Asset Management, Inc., 829 F.2d 1209 (2d Cir.1987) (pierced corporate veil so as to hold shareholders jointly and severally liable with the corporations for fiduciary breaches); Board of Trustees of Teamsters Local 863 Pension Fund v. Foodtown, Inc., 296 F.3d 164 (3d Cir. 2002) (summary judgment to dismiss piercing corporate veil claim by multiemployer pension fund against individual defendants not granted; noted that under N.J. law to pierce corporate veil must show that: (i) the corporation is organized and operated as a mere instrumentality of the other corporation and (ii) the dominant corporation uses the subservient corporation to penetrate fraud, to accomplish injustice or to circumvent the law; with factors to be considered including the failure to observe corporate formalities and non-functioning of other officers and directors); Reilly v. Reem Contracting Corp., 380 Fed. Appx. 16 (2d Cir. 2010; unpublished) (plumbing company alter-ego of contracting company and liable for contributions to union benefit funds); Resilient Floor Covering Pension Fund v. M & M Installation, Inc., 630 F.3d 848 (9th Cir. 2010) (non-union company may be liable for withdrawal liability of union company where there was a commonality between union and non-union firms and an abuse of the union/non-union structure to avoid payment of withdrawal liability); Trustees of Operating Engineers Local 324 Pension Fund v. Bourdow Contracting, Inc., 919 F.3d 368 (6th Cir. 2019) (a newly-formed LLC was held to be alter ego of a bankrupt company that was a signatory to a collective bargaining agreement and was liable to the union’s pension fund).

See, however, the following court cases which did not pierce the corporate veil: Reich v. Compton, 57 F.3d 270 (3d Cir.1995) (refusing to impose liability for prohibited transaction on alter ego of party in interest under federal common law of ERISA); United Union of Roofers, Waterproofers, and Allied Workers Local No. 210, AFL-CIO v. A.W. Farrell & Son, Inc., 547 Fed. Appx. 17 (2d Cir. 2013) (the Second Circuit held that two businesses that were affiliated and owned by different family members but were not members of the same controlled group should not be treated as a single employer for purposes of joint withdrawal liability from a multiemployer pension plan; the court considered the following factors in making its determination: (i) interrelation of operations, (ii) management, (iii) centralized control of labor relations, (iv) common ownership, (v) the use of common office facilities and equipment, and (vi) family connections between and among the various enterprises).

[19] When TWA entered bankruptcy with two pension plans underfunded by $1.2 billion, the PBGC threatened to pursue Carl Icahn, the 80% shareholder of TWA and his other corporations. Carl Icahn reached an agreement with the PBGC to make loans and guarantees to the plans to keep them operating. See, N.Y. Times, Dec. 8, 1992, p. D-5. Also, in 2006, in connection with the bankruptcy of one of the plants of R.G. Steel, which had a $100 million underfunded pension plan, the PBGC filed a lawsuit against the parent, Renco Group seeking to a lien on its assets as well as on the Hamptons estate of Renco Group’s founder, and the PBGC settled with the Renco Group after it agreed to continue to be liable for the underfunded plan and contribute $20 million to it. NY Times, April 1, 2006. In 2012 the PBGC filed a suit in the S.D.N.Y. in connection with the bankruptcy of R.G. Steel, a subsidiary of Renco Group, alleging that Renco Group entered into a transaction with a principal purpose of evading $97 million unfunded benefit liabilities, unpaid minimum funding contributions and termination premiums. BNA Pen. & Ben. Rptr. (Feb. 5, 2013). In 2016 Renco settled with the PBGC to restore the pension plans of 1,350 retirees of RG Steel. NY Times, March 4, 2016.

[20] C.I.R. v. Groetzinger, 480 U.S. 23, 35, 107 S. Ct. 980, 987, 94 L. Ed. 2d 25 (1987). This is applied in the ERISA context by, e.g., Central States, Southeast and Southwest Pension Fund v. Personnel, Inc., 974 F.2d 789 (7th Cir. 1992); Connors v. Incoal, Inc., 995 F.2d 245 (D.C. Cir. 1993).

[21] The Groetzinger case is applied in the ERISA context by, e.g., Central States, Southeast and Southwest Pension Fund v. Personnel, Inc., 974 F.2d 789 (7th Cir. 1992) and Connors v. Incoal, Inc., 995 F.2d 245 (D.C. Cir. 1993).

[22] E.g., Central States, Southeast and Southwest Pension Fund v. Personnel, Inc., 974 F.2d 789 (7th Cir.1992) (no nexus required to show ERISA affiliation; corporation withdrawing from a multiemployer pension plan, where the corporation’s sole shareholder held certain real estate investments, withdrawal liability could be imposed on the sole shareholder since the real estate investment leasing activities constituted a trade or business); Connors v. Incoal, Inc., 995 F.2d 245 (D.C. Cir. 1993) (no economic nexus required for determining trade or business under ERISA; a corporation which withdrew from a multiemployer pension plan, which was owned by a family that also held the partnership interests in a farm could cause the shareholder to be liable); Pension Ben. Guar. Corp. v. Center City Motors, Inc., 609 F. Supp. 409 (S.D. Cal. 1984) (genuine issue of material fact existed as to whether rental property proprietorship was a trade or business); Board of Trustees of Western Conference of Teamsters Pension Trust Fund v. Lafrenz, 837 F.2d 892 (9th Cir. 1988) (unincorporated truck leasing operation of husband and wife was a trade or business, and thus affiliated with a commonly controlled corporation that withdrew from a multiemployer plan); Central States, Southeast & Southwest Areas Pension Fund v. Neiman, 285 F.3d 587 (7th Cir. 2002) (the owner of a defunct trucking company was personally liable for the trucking company’s multiemployer withdrawal liability because he had an unincorporated trade or business of providing consulting services to a real estate management company and to a subsidiary trucking company); Minnesota Laborers Health and Welfare Fund v. Scanlan, 360 F.3d 925 (8th Cir. 2004) (owner personally liable to multiemployer plan where he signed collective bargaining agreement as owner of an unincorporated business, and not merely as an officer of one of the other unincorporated entities); Central States, Southeast and Southwest Areas Pension Fund v. SCOFBP, LLC, 668 F.3d 873 (7th Cir. 2011), cert. denied, 566 U.S. 1022 (2012) (where an entity ceased making contributions to a multiemployer plan, that two other entities were under common control were also liable; the owner of all three entities filed for personal bankruptcy and the entities, which were limited liability companies, were subject to the individual’s ownership; the two affiliated companies were engaged in a trade or business by virtue of their regularly leasing real estate holdings to other entities and were not mere passive investment vehicles and were all subject to multiemployer withdrawal liability); Central States, Southeast and Southwest Areas Pension Fund v. Messina Products, LLC, 706 F.3d 874 (7th Cir. 2013) (a husband and wife who owned a trucking company that incurred ERISA withdrawal liability for withdrawing from a multiemployer pension plan were held personally liable for the withdrawal liability since the individual owners were engaged in a trade or business by renting several properties to the trucking company and were not merely passive investors, since renting property to one’s own business is activity for the primary purpose of income or profit performed with continuity and regularity under the Groetzinger test); Central States, Southeast and Southwest Areas Pension Fund v. Nagy, 714 F.3d 545 (7th Cir. 2013) (company ceased employing covered workers and incurred ERISA withdrawal liability; court held that the individual owner of the company is liable for withdrawal liability since the individual owner leased property to the company; therefore the individual owner was engaged in a trade or business); Pension Benefit Guaranty Corporation v. Findlay Industries, Inc., et al., 902 F.3d 597 (6th Cir. 2018) (the court held that a family was personally liable for the underfunding of a pension plan; a privately owned business was under the control of the family; the court held that the family was personally liable for the underfunding for the commonly controlled entities; that also made the entities liable for successor liability under ERISA § 4069(a) for transactions entered into to avoid liability); Local No. 499, Board of Trustees of Shopmen’s Pension Plan v. Art Iron, Inc., 117 F.4th 923 (6th Cir. 2024) (multiemployer pension plan sought withdrawal liability, after Art Iron, Inc. withdrew from the plan, from the company, as well as from its sole shareholder Robert Schlatter and his wife Mary Schlatter; court stated that a trade or business depends on the continuity and regularity of the activity and whether it was primarily for income or profit; court held that Robert Schlatter consulting work for the company, which occurred over a number of years, including the year of pension withdrawal, was a trade or business and therefore he could be held personally liable for the company’s withdrawal liability; but his wife’s jewelry business was not a trade or business since it was not operated with regularity and continuity and therefore she was not liable).

But see, Textile Workers Pension Fund v. Oltremare, 764 F. Supp. 287 (S.D.N.Y. 1989) (mere ownership of real property without economic nexus to commonly controlled entity not enough to constitute trade or business); Central States, Southeast and Southwest Areas Pension Fund v. Fulkerson, 238 F.3d 891 (7th Cir. 2001), cert. denied, 534 U.S. 821 (bankrupt trucking company owner’s other leasing activities were merely passive holdings for investment and not a trade or business for purposes of controlled group multiemployer withdrawal liability); Central States, Southeast and Southwest Areas Pension Fund v. White, 258 F.3d 636 (7th Cir. 2001) (bankrupt trucking company owner’s apartment rental activities were not a “trade or business” under ERISA § 4001(b)(1) for purposes of multiemployer withdrawal liability).

[23] C.I.R. v. Groetzinger, 480 U.S. 23, 35 (1987), cited above.

[24] PBGC Appeals Board Opinion dated Sept. 26, 2007, www.pbgc.gov/prac/appeals-board/appeals-decisions (a single private equity fund owned 80% or more of a portfolio company, and the portfolio company was liable to the PBGC for pension termination liability; the issue was whether the private equity fund was a “trade or business” under the standard set forth in Groetzinger that “trade or business” depends on (i) whether the taxpayer is engaged in an activity with the primary purpose of income or profit, and (ii) whether the act is conducted with continuity and regularity; in the facts of that letter the private equity fund engaged in an activity with the primary purpose of income or profit, and it conducted its business through an agent (the general partner) who managed the fund’s investments on a regular basis; the private equity fund was therefore held to be in the same controlled group as the portfolio company that sponsored a pension plan).

[25] See ABA JCEB Q & As for PBGC (May 2008), Q & A 11, that it is likely that a private equity fund would be a trade or business, absent unusual facts and circumstances.

[26] Board of Trustees, Sheet Metal Workers National Pension Fund v. Palladium Equity Partners, LLC, 722 F. Supp. 2d 854 (E.D. Mich. 2010) (genuine issue of material fact existed as to whether three Palladium limited partnerships, as well as Palladium Equity Partners, LLC which served as advisor, were an ERISA controlled group parent liable for ERISA multiemployer withdrawal liability of the Haden group of companies; the court found the 2007 PBGC Appeals Board Opinion to be persuasive that although investment alone is not a trade or business, where there is “investment plus,” e.g., investment advisory and management services by the fund for the benefit of its partners and compensation for the investment advisory and management services, this would constitute a trade or business; court found there was a genuine issue of material fact as to whether the Palladium funds had a business purpose other than merely investment; the Palladium funds joined their investments to exert power over financial and managerial activities of the portfolio companies, selected five of the seven board members and set up several committees to control the internal operations of the portfolio companies; in terms of considering the four partnerships as a single partnership for the parent-subsidiary controlled group test, the court stated that there was a genuine issue of material fact as to whether the three LP funds constituted a partnership or joint venture in fact under the Luna standards discussed below; the facts before the court did not clearly establish whether the Palladium entities acted as a joint venture or partnership concerning their portfolio companies; the terms of their agreement and their conduct must be analyzed; there was also general issue of material fact regarding alter-ego liability).

[27] Longroad Asset Management LLC v. Boilermaker Blacksmith National Pension Trust, No. 4:23-cv-00738-DGK 2025 WL 2406740 (W.D. Missouri Aug. 19, 2025) (Longroad Capital Partners III, LP (“Longroad LP”) set up a 95% controlled subsidiary Broad Street Tank Holding Co., Inc. (“Broad Street”) in order to acquire through the purchase of the outstanding debt and receipt of all the assets of the distress company Brown-Minneapolis Tank – Northwest, LLC (“BMT-NW”), through a special entity BMT -NW Acquisition; in addition, Broad Street acquired Graver Tank Co. Both BMT-NW Acquisition and Graver Tank Co. went bankrupt and thereby withdrew from the multiemployer pension plan; the court held that the Longroad LP and its 95% controlled Broad Street were a trade or business under the investment-plus analysis and were jointly and severally liability for the withdrawal of their portfolio companies BMT-NW Acquisition and Graver that went bankrupt; the asset manager and general partner were not part of the controlled group).

[28] Luna v. C. I. R., 42 T.C. 1067 (1967) (a lump-sum settlement payment received by petitioner from an insurance company, Pioneer Life & Casualty Co., in settlement of petitioner’s right to receive renewal commissions on special type insurance policies, conceived by termination of petitioner’s employment contract with the insurance company, was taxable to petitioners as ordinary income; court concluded that petitioner and Pioneer were not partners or joint venturers and that no part of the lump-sum settlement paid to petitioner was proceeds from the sale or exchange of an interest in a of a capital asset or an interest in a joint venture or partnership and it could not be taxed as a capital gain).

[29] Sun Capital Partners III, LP v. New England Teamsters & Trucking Industry Pension Fund, 724 F.3d 129 (1st Cir. 2013), cert. denied, 134 S. Ct. 1492 (2014) (two private equity funds managed by Sun Capital, Sun Fund III and Sun Fund IV owned 70% and 30%, respectively, of Scott Brass, Inc. which withdrew from a multiemployer pension plan prior to filing for bankruptcy; the district court at 903 F.Supp.2d 107 (D. Mass. 2012), had granted the Sun Capital Partners equity funds’ motion to dismiss since the private equity funds were passive investors and not a trade or business and the 2007 PBGC Appeals Board Opinion was unpersuasive because activity of the general partner should not have been attributed to the investment fund and continuity and regularity of an activity should not be found merely based on the size of the investment and profitability; however, the First Circuit reversed and held that at least the larger of the two Sun funds (Fund IV) was engaged in a trade or business under an “investment plus” analysis since there was more than mere passive investment, noting that the funds sought out potential portfolio companies that were in need of extensive management intervention, the general partners of the funds had wide-ranging management authority, the funds had the power to appoint a majority of board members, the general partners of the funds could make decisions regarding hiring, termination and compensation of employees in the portfolio companies, and at least with respect to Sun Fund IV (the 70% owners) the active investment in management provided a direct economic benefit that an ordinary passive investor would not derive, i.e., management fees the fund otherwise would have needed to pay its general partner of the fund was offset by fees the portfolio company was paying to the general partner; thus Fund IV and possibly Fund III were a trade or business; the purchase of Scott Brass, Inc. in a 70%-30% split was not done with a principal purpose to evade or avoid liability under ERISA § 4212(c), because disregarding a 70%-30% split would leave zero ownership; the court, however, remanded the case to the district court to determine if Fund III was also a trade or business and to determine if there was common control by the 70%-30% ownership by reason of being considered a partnership in fact).

[30] Sun Capital Partners III, LP v. New England Teamsters and Trucking Industry Pension Fund, 172 F. Supp. 3d 447 (D. Mass. 2016) (on remand, the district court held: (i) that under the “investment plus” analysis not only was Sun Fund IV a trade or business, but Sun Fund III was also a trade or business because it too had a direct economic benefit that a passive investor would not have, i.e., an offset of fees otherwise owed by Sun Fund III to its general partner for managing the investments indirectly paid by the underlying company; and (ii) with regard to common ownership of SBI, while not specifically meeting the requirements for an ERISA controlled group because there was no 80% controlling interest, nevertheless Sun Fund III and Sun Fund IV are a jointly controlled entity where there was a deemed) partnership-in-fact under tax-law principles since the two funds often co-invest together, and the general partners were controlled by the same two people, and despite the lack of permanently fixed co-investing, these Sun Funds should be considered as joining together as a “partnership-in-fact” to invest in Scott Brass; the district court noted that the fund split in ownership was done because the fund was nearing the end of its investment cycle, a preference for income diversification and a desire to keep ownership below 80% to avoid ERISA withdrawal liability (though avoiding controlled group liability was not the principal purpose of the transaction for purposes of ERISA § 4212(c)).

Some have questioned the partner-in-fact theory for controlled group liability because (i) partnership-in-fact is tax law or state-law concept that may not automatically apply to ERISA controlled group liability situations, and (ii) the bright line ERISA controlled group test was being expanded in a way not contemplated by the statute or regulations, or by ERISA § 4212(c).

[31] Sun Capital Partners III, LP v New England Teamsters & Trucking Industry Pension Fund, 943 F.3d 49 (1st Cir. 2019), cert. denied, 141 S. Ct. 372 (2020) (court found that private equity funds did not form a partnership-in-fact to acquire SBI under Code § 7701(a)(2) because a number of factors in the Luna test had not been met since (i) the funds disclaimed any sort of partnership, (ii) most of the entities or persons who were limited partners in Sun Fund IV were not limited partners in Sun Fund III, (iii) separate tax returns, separate books and separate bank accounts were maintained and (iv) the funds did not operate in parallel, i.e., they did not invest in the same companies at a fixed or even variable rate, which shows some independence in activity and structure; therefore the court held that the funds; therefore most of the Luna factors were not met; also there is not a firm indication of Congressional intent that withdrawal liability would be imposed on these private investors absent guidance from the PBGC; therefore the funds are not jointly liable for the ERISA withdrawal liability).

[32] In certain cases, it may be advisable to specify in agreements with representations about controlled group members that representations are (or are not) made with regard to private equity investors and other portfolio companies.