Mandatory Roth Catch-Up Contributions Took Effect January 1, 2026

By Charles C. Shulman

Mandatory Roth catch-up contributions took effect on January 1, 2026, fundamentally changing the operation of age-50 “catch-up” contributions for higher-wage employees. Under final IRS and Treasury regulations implementing SECURE 2.0, catch-up contributions for participants whose prior-year wages exceeded a statutory threshold ($150,000 when first applied in 2026) must be made on a Roth (after-tax) basis. Although Congress originally scheduled this change to apply beginning in 2024, the IRS delayed mandatory implementation until 2026 and provided employers additional time—generally through the end of the 2027 plan year—to complete conforming plan amendments. As of 2026, however, plans offering catch-up contributions are required to operate in compliance with the Roth-only requirement, and employers must maintain appropriate payroll, recordkeeping, and administrative procedures.

I. Overview

The IRS and Treasury have implemented IRC §414(v)(7) through final regulations, T.D. 2025-17865, 90 Fed. Reg. 2645 (Sept. 16, 2025), fundamentally altering how age-50 catch-up contributions operate for higher-wage participants. Although the statute originally provided that mandatory Roth catch-up contributions would apply to taxable years beginning after December 31, 2023, subsequent IRS transition relief postponed operational enforcement. As a result, mandatory Roth-only catch-up contributions became effective for taxable years beginning after December 31, 2025, and therefore apply beginning January 1, 2026.

While the final regulations provide that full regulatory compliance is required beginning in 2027, plans have been permitted to rely on reasonable, good-faith interpretations through the 2026 transition period. This memorandum summarizes the catch-up contribution framework as it now applies, explains the Roth-only mandate currently in effect, and outlines the remaining amendment and compliance deadlines.

II. Background: Catch-Up Contributions Under §414(v)

Under IRC §414(v), individuals who are age 50 or older (or who will attain age 50 by the end of the taxable year) may make additional “catch-up” contributions beyond the §401(a)(30)/§402(g) elective deferral limits. These limits have increased over time, reaching $8,000 for 2026 for §401(k) and §403(b) plans. Catch-up contributions remain exempt from the ADP test, the §415(c) annual addition limits, and the top-heavy rules for the year made. Although plans are not required to offer catch-up contributions, those that do must satisfy the “universal availability” requirement of Treas. Reg. §1.414(v)-1(e), under which all catch-up-eligible participants must have the same effective opportunity to make them. The SECURE 2.0 Act also introduced enhanced catch-up limits for participants ages 60–63 beginning in 2025. Those enhanced limits equal the greater of $10,000 (indexed after 2025) or 150% of the regular catch-up amount; SIMPLE catch-ups increase by 10% beginning in 2025.

III. SECURE 2.0 Roth Catch-Up Mandate

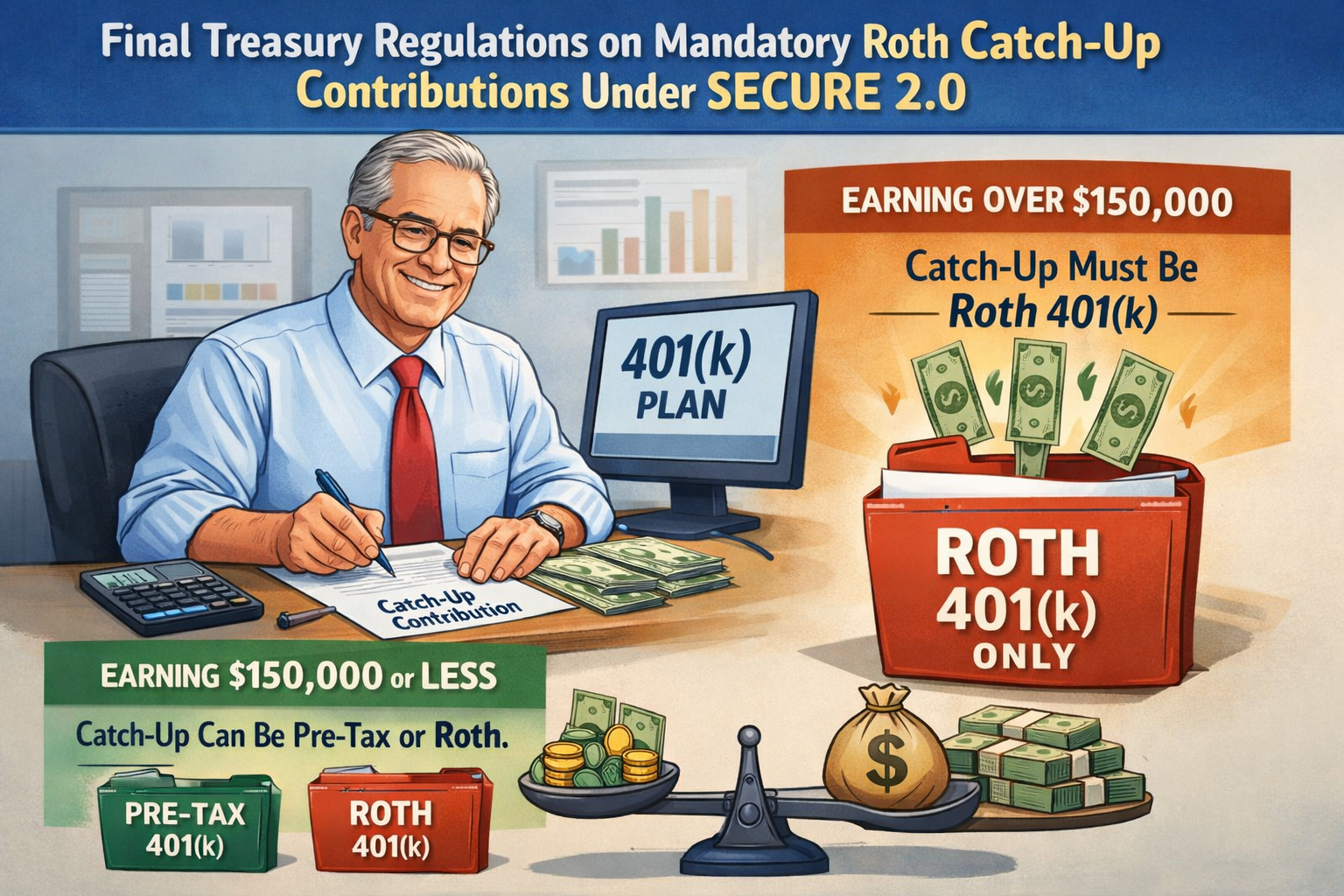

Section 603 of SECURE 2.0 added IRC §414(v)(7), which now requires that catch-up contributions for participants with prior-year FICA wages above a statutory threshold must be made as designated Roth contributions. For 2023–2025, the statutory threshold is $145,000, and beginning in 2026 the threshold is indexed in $5,000 increments (increased to $150,000 for determinations made in 2026 based on 2025 wages). The Roth mandate applies to §401(k), §403(b), and governmental §457(b) plans; SIMPLE IRAs and SEPs are excluded.

Although the statutory effective date was originally set for taxable years beginning after December 31, 2023, IRS Notice 2023-62 delayed the mandatory application of §414(v)(7) for two years. As a result, participants are not required to make Roth-only catch-up contributions in 2024 or 2025. The final regulations confirm this transition relief and provide that the Roth-only mandate first became operationally required for taxable years beginning after December 31, 2025—meaning the first year in which plans must enforce Roth-only catch-ups is 2026.

IRS Notice 2023-62 allowed a “reasonable, good-faith” interpretation of §414(v)(7) during 2024–2026. The final regulations become mandatory beginning in 2027, unless a plan elects early adoption.

IV. Key Features of the Final Regulations and Their Effective Dates

The final regulations at Treas. Reg. §1.414(v)-2 and related amendments define and govern who is subject to the Roth-catch-up requirement, how the rule applies in operation, and what correction and administrative procedures are necessary. The following aspects are most relevant for plan sponsors, together with the associated timing considerations.

Who is subject to the Roth-catch-up requirement. Under Treas. Reg. §1.414(v)-2(a)(2), a participant is subject to the Roth-only mandate if the participant is otherwise catch-up-eligible and had FICA wages from the employer sponsoring the plan that exceeded the applicable threshold for the preceding calendar year. The test is mechanical and employer-specific. A participant who exceeds the wage threshold based on 2025 wages must make all 2026 catch-up contributions on a Roth basis.

Optional wage aggregation rules. Under Treas. Reg. §1.414(v)-2(b)(4), plans may elect, but are not required, to aggregate FICA wages across (i) employers using a common paymaster, (ii) employers in a controlled group or affiliated service group, or (iii) predecessor and successor employers in an asset transaction. If the plan does not elect aggregation, wages are tested separately for each employer, even within a single multiple-employer plan.

Scope of Roth requirement and interaction with elective deferral limits. The Roth mandate applies only to elective deferrals that qualify as catch-up contributions under Treas. Reg. §1.414(v)-1(c)(3). Higher-wage participants may still make pre-tax elective deferrals up to the §401(a)(30)/§402(g) limit; Roth treatment becomes mandatory only when elective deferrals exceed that limit. The final regulations clarify that earlier designated Roth contributions count toward satisfying the Roth requirement, thus avoiding an “all-or-nothing” Roth conversion.

Universal availability rules and high-wage participants. The final regulations clarify that a plan does not violate universal availability merely because it does not permit catch-up contributions for participants who exceed the wage threshold. In practice, one plan in a controlled group may offer full Roth catch-ups while another may deny catch-ups entirely to high-wage participants, without violating Treas. Reg. §1.414(v)-1(e).

Deemed Roth catch-up elections. Under Treas. Reg. §1.401(k)-1(f)(5), plans may use deemed Roth elections for participants subject to §414(v)(7), provided participants retain an effective opportunity to make alternative elections. Deemed elections must cease once a participant is determined not to exceed the wage threshold or once the employer receives a corrected Form W-2.

Plans lacking a Roth contribution feature. Under Treas. Reg. §1.414(v)-2(b)(2), if a plan does not include a Roth contribution program under §402A(b), a participant subject to the Roth requirement has a maximum catch-up limit of zero. Sponsors wishing to preserve catch-ups for higher-wage employees must therefore add a Roth feature before 2026.

Correction mechanisms. Treas. Reg. §1.414(v)-2(c) establishes correction rules for operational failures, including (i) recharacterization and corrected Form W-2 reporting before issuance, or (ii) in-plan Roth rollovers reported on Form 1099-R. Plans using these correction methods must include a deemed Roth catch-up election in their plan documents. Relief applies to de minimis failures not exceeding $250 and failures resulting from late amended Forms W-2.

V. Effective Dates and Required Amendments

The interaction of statutory language, IRS transition relief, and regulatory applicability yields the following compliance timeline: The Roth-only requirement under §414(v)(7) did not apply in 2024 or 2025 as a result of the administrative transition in IRS Notice 2023-62. The first year in which plans must require Roth-only catch-up contributions is 2026, based on 2025 FICA wages. The final regulations apply mandatorily to taxable years beginning after December 31, 2026; therefore, 2027 is the first year in which plans must comply with the detailed regulatory framework unless the plan elects early reliance for 2024–2026 under Treas. Reg. §1.414(v)-2(e)(2)(iv). Plan amendments implementing §414(v)(7), including the deemed election provisions and optional wage aggregation rules, must generally be adopted by the end of the 2027 plan year. Governmental plans have until the end of the 2029 plan year.

As a result, plan sponsors may operate under a reasonable, good-faith interpretation of §414(v)(7) through 2026, even if full regulatory language has not yet been added to the plan, so long as 2026 operations correctly enforce Roth-only treatment for participants exceeding the wage threshold.

VI. Action Steps for Plan Sponsors

Plan sponsors should by now have completed, or should be completing, preparations for the 2026 Roth-only operational mandate. Employers should (i) adopt a Roth contribution feature if catch-up contributions are to remain available to higher-wage participants beginning in 2026; (ii) coordinate with payroll providers to ensure accurate prior-year FICA wage determinations; (iii) update participant communications and election materials before the 2026 plan year; (iv) evaluate controlled group practices, since different plans may permissibly take different approaches for high-wage participants; (v) implement operational procedures for deemed Roth elections and correction methods during the 2026–2027 transition period; and (vi) ensure plan amendments are completed by the end of the 2027 plan year (or 2029 for governmental plans).

VII. Conclusion

The September 2025 final regulations marked the most significant changes to catch-up contribution administration in more than a decade. Plan sponsors should be operating Roth-only catch-up contributions, which began in 2026, and should ensure that Roth features, deemed election language, and correction procedures are in place well before the 2027 regulatory applicability date. Continued coordination with payroll and recordkeepers will be essential to ensure smooth operation and ongoing compliance.